In Nepal, Fixed Deposits (FDs), or Mudhati Khata, are widely regarded as the safest and most reliable investment option. Whether for a secure retirement or saving for future goals, many Nepali people trust FDs because they offer guaranteed returns without the risks associated with the stock market.

However, simply knowing the interest rate offered by the bank is not enough. Many depositors often find themselves confused about how FD interest is calculated, especially when it comes to tax deductions and the difference between monthly and yearly payouts. Understanding these details is crucial to knowing exactly how much your money will grow over time.

In this guide, we will simplify the process for you. We will explain how to calculate fixed deposit interest with clear formulas, break down different payout methods, and provide real-life examples so you can plan your finances with confidence. So, let us get started!

A Fixed Deposit (FD), or Mudhati Khata, is a popular and secure way to invest in Nepal. You put a lump sum of money in a bank or financial institution for a set period, and they give you a guaranteed interest rate, usually higher than a regular savings account.

Why do banks offer higher rates for FDs? It’s because FDs give banks stability. Unlike savings accounts, FDs lock your money for a set time, so banks can use it for long-term loans. In return for keeping your money with them, banks offer you better returns.

Banks in Nepal offer FDs for many different time periods. You can choose a short-term FD for 3 or 6 months, or a long-term one for 1, 2, or even 10 years. Usually, the longer you keep your money in an FD, the higher the interest rate you get. This makes FDs a good choice for careful investors.

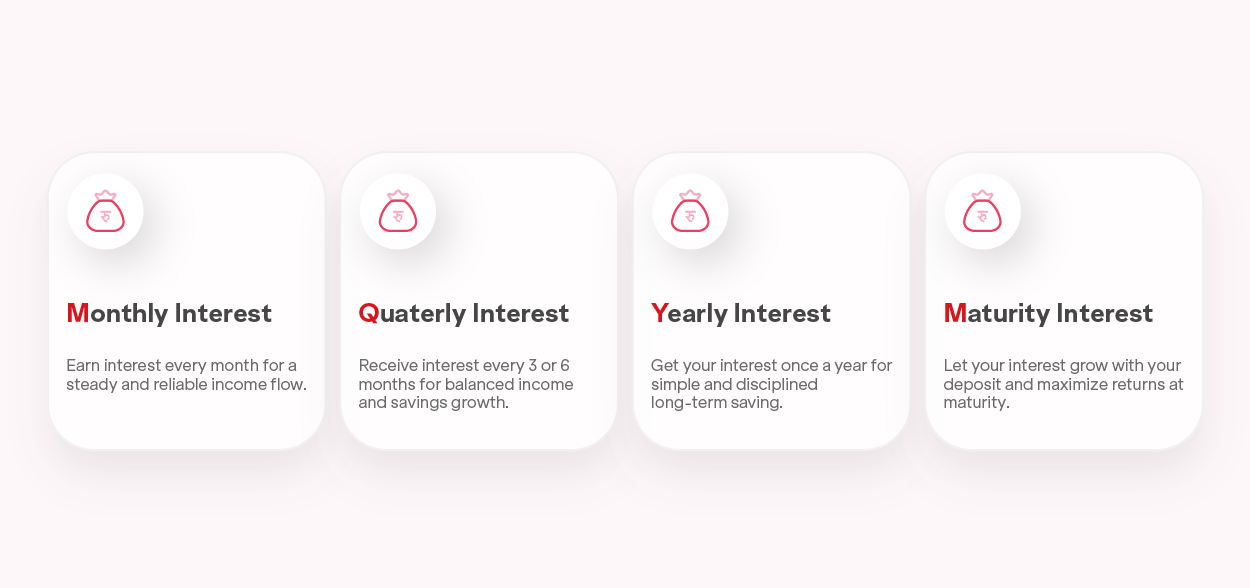

When you open a Fixed Deposit (FD), it’s important to know how the interest will be paid. The payout method can affect your financial planning. Here are the common ways banks in Nepal pay FD interest:

If you need a steady income, the Monthly Interest Payout FD is a good option. The bank credits the interest to your savings account every month. This is popular with retirees and people who want to use the interest for daily expenses or to add to their monthly income.

This is the most common payout method in Nepali banks. Here, interest is paid every three months (quarterly) or every six months (half-yearly). It offers a balance between regular income and growing your investment, making it a good choice for people with occasional financial needs or short-term plans.

If you don’t need to use your interest often, the Yearly Interest Payout FD is a smart choice. The bank credits the interest once a year. This suits long-term investors who want to collect their earnings yearly instead of spending them throughout the year.

If you want to grow your wealth, the Maturity Interest FD is a strong option. Instead of getting interest payouts during the term, the interest is added to your principal, so you earn interest on a bigger amount each time. This compounding effect can greatly increase your total returns, making it ideal for long-term growth.

For most Fixed Deposits in Nepal that last a year or less, banks use the Simple Interest Method to figure out your earnings. This formula is easy to use and lets you quickly estimate your returns without worrying about compounding.

Here is the formula you need to know:

Interest = (Principal × Rate × Time) / 100

Where:

Let’s see this formula in action with a practical example.

Let’s look at a practical example to see how this formula works.

Suppose you decide to deposit Rs. 100,000 in a Fixed Deposit for 1 year at an annual interest rate of 10%.

Using the formula: Interest = (100,000 × 10 × 1) / 100

Interest = Rs. 10,000

So, at the end of the year, your total maturity amount will be: Final Maturity Amount = Principal + Interest

Final Maturity Amount = Rs. 100,000 + Rs. 10,000 = Rs. 110,000

This calculation shows you how much your money can grow in a year, which helps you plan your finances more easily.

Apart from the longer duration FDs, banks in Nepal also allow you to open a Fixed Deposit for a shorter period of time, like 3 months or 6 months. In such cases, the standard Simple Interest formula needs a small adjustment to account for the partial year.

Here is how banks calculate interest for FDs with durations less than a year:

To calculate FD interest for a certain number of months, just divide the number of months by 12 to get the time in years.

Time (T) = Number of Months / 12

Let's say you decide to deposit Rs. 200,000 in a Fixed Deposit for a period of 3 months at an annual interest rate of 9%.

First, calculate the time in years:

Time (T) = 3 / 12 = 0.25 years

Now, plug this into the formula:

Interest = (200,000 × 9 × 0.25) / 100

Interest = Rs. 4,500

So, after 3 months, your total maturity amount will be:

Final Maturity Amount = Rs. 200,000 + Rs. 4,500 = Rs. 204,500

Now, imagine you deposit Rs. 500,000 in a Fixed Deposit for a period of 6 months at an annual interest rate of 8.5%.

Calculate the time in years: Time (T) = 6 / 12 = 0.5 years

Using the formula: Interest = (500,000 × 8.5 × 0.5) / 100

Interest = Rs. 21,250

After 6 months, your total maturity amount will be: Final Maturity Amount = Rs. 500,000 + Rs. 21,250 = Rs. 521,250

With these simple steps, you can easily estimate your returns, even for short-term FDs.

If you pick a Cumulative Fixed Deposit or want to get your interest at maturity, the simple interest formula won’t show the full picture. In these cases, you need to use compound interest.

Compounding means earning interest on your interest. Instead of getting your interest every quarter, the bank adds it to your principal. This way, in the next quarter, you earn interest on a bigger amount. Over time, this can greatly increase your total returns.

To find the maturity amount with compounding, use this formula. It may look complicated, but it becomes easy once you put in the numbers.

Maturity Amount (A) = P (1 + r/n)^(nt)

Where:

Most banks in Nepal compound interest every quarter, or four times a year. Let’s see how a deposit of 1 Lakh grows over 2 years.

Given: Principal (P) = Rs. 100,000

Annual Interest Rate (r) = 10% (0.10)

Time (t) = 2 years

Compounding Frequency (n) = 4 (Quarterly)

Calculation Steps:

Step 1: Set up the formula

First, we divide the annual rate by the compounding frequency: r/n = 0.10 / 4 = 0.025

Next, we determine the total number of compounding periods: n × t = 4 × 2 = 8

Now, the formula looks like this: A = 100,000 × (1 + 0.025)^8

A = 100,000 × (1.025)^8

Step 2: Calculate the power value

Using a calculator, we find the value of (1.025)^8:

(1.025)^8 ≈ 1.2184

Step 3: Multiply by the Principal

A = 100,000 × 1.2184

Maturity Amount (A) = Rs. 121,840

Final Result: So after 2 years, your total maturity amount will be Rs. 121,840.

To find out exactly how much profit you made: Total Interest Earned = Maturity Amount (A) - Principal (P)

Total Interest = 121,840 - 100,000 = Rs. 21,840

(Note: Quarterly compounding is common, but some banks in Nepal may use semi-annual or annual compounding. Always check your FD’s terms.)

When you calculate your Fixed Deposit returns, don’t forget about taxes. The interest rate shown by the bank (like 9.5%) is the gross rate, but you won’t get the full amount in your account.

In Nepal, interest earned from any bank deposit, including Fixed Deposits, is subject to a 6% Tax Deducted at Source (TDS) for individuals. This means the bank automatically deducts 6% of your total interest earnings and pays it to the government before crediting the remaining amount to your account.

So, if you calculated that you would earn Rs. 10,000 in interest, you won't get the full amount. The bank will deduct Rs. 600 (6% of 10,000) as TDS, and your actual Net Interest Income will be Rs. 9,400.

Keep this in mind when planning: your final maturity amount will be a bit less than the gross calculation because of the tax deduction. For institutions, the tax is 15%, but for individual savers, it’s a flat 6%.

Let’s face it, no one wants to pull out a calculator every time they think about saving money. To make things easier, we have compiled a quick reference table showing the Gross Interest, Tax Deductions, and the final Maturity Amount for common deposit scenarios.

This table assumes a standard 6% TDS deduction on interest earnings (as per current regulations for individuals).

| Principal Amount (Rs.) | Interest Rate | Duration | Gross Interest (Rs.) | Net Interest After 6% Tax (Rs.) | Total Maturity Amount (Rs.) |

| 100,000 | 10% | 1 Year | 10,000 | 9,400 | 109,400 |

| 200,000 | 9% | 1 Year | 18,000 | 16,920 | 216,920 |

| 500,000 | 10% | 1 Year | 50,000 | 47,000 | 547,000 |

| 1,000,000 | 11% | 1 Year | 110,000 | 103,400 | 1,103,400 |

| 1,500,000 | 10.50% | 2 Years | 315,000 | 296,100 | 1,796,100 |

Note: The actual interest rate and tax policy may vary based on bank schemes and government regulations. Always verify the latest rates before opening an FD.

When planning your Fixed Deposit, you may wonder whether to calculate interest yourself or use an online tool. Both have their benefits. Here’s a look at the pros and cons of manual calculation versus using an FD calculator.

Calculating FD interest by hand helps you understand how your money grows. Working through the formula shows you the difference between simple and compound interest, which can help you make better financial decisions.

Here is why manual calculation is beneficial:

But manual calculation can lead to mistakes, especially with compounding and taxes. An online FD calculator makes things easier by giving you accurate results quickly.

Here is why you should use an online tool:

Manual calculation is useful for learning or quick estimates. But when you want to make a real investment, it’s best to use an FD Calculator. It saves time, avoids mistakes, and shows you your earnings after tax.

Want to know your exact returns? Try our FD Calculator for Nepal. It uses the latest interest rates from all major banks and adjusts for tax, so you can make the best investment choice right away.

When comparing Fixed Deposits, it might seem like all 10% interest rates give the same return. But in reality, your earnings depend on several factors that can vary between banks. Knowing these details can help you get the most from your investment.

Here are the key factors that influence how much interest you will earn on your FD in Nepal:

Choosing the right Fixed Deposit isn’t only about getting the highest interest rate. It’s also about matching your investment to your financial needs. For example, a retiree may want a monthly income, while a young professional might be saving for a house. Your goal should guide your choice.

Here is a practical guide to help you pick the best FD option for your needs:

If you use your savings for daily expenses, like many retirees or freelancers, choose a Monthly or Quarterly Payout FD. The interest goes straight to your savings account, giving you regular income without using your principal.

If your goal is to grow your wealth, pick a Cumulative (Compounded) FD. When you reinvest your interest, you benefit from compounding. Over a few years, this effect can greatly increase your total maturity amount compared to regular payouts.

If you have a goal, like buying a car in 3 years or paying for a child’s education in 5 years, consider a Long-Term FD. These usually offer higher interest rates and help you save by making it harder to withdraw money early.

When interest rates are rising, as they sometimes do in Nepal, avoid locking your money for too long. Instead, use a Short-Term FD. Deposit for 6 months or 1 year, then renew at the new, higher rate when your FD matures. This way, you can get better returns.

Fixed deposit interest rates in Nepal are changing frequently as the banking system adjusts to excess liquidity and shifting monetary policy. While the weighted average deposit rate currently hovers around 3.66%, actual rates vary significantly across banks and deposit tenures. A rate that looked attractive last month may no longer be the best option today.

That's why comparing rates regularly matters. To find out which bank is offering the best FD rate right now, check our bank-wise FD interest rate comparison and make your savings decision based on the latest data.

| S.N. | Bank Name | Interest Rate |

| 1 | Garima Bikas Bank | 5.43% |

| 2 | Muktinath Bikas Bank | 5.15% |

| 3 | Mahalaxmi Bikas Bank | 5.15% |

| 4 | Lumbini Bikas Bank | 5.11% |

| 5 | Jyoti Bikas Bank | 5.11% |

| 6 | Shine Resunga Development Bank | 5.11% |

| 7 | Kamana Sewa Bikas Bank | 5.11% |

| 8 | Shangri-la Development Bank | 5.11% |

| 9 | Himalayan Bank | 5% |

| 10 | Rastriya Banijya Bank | 5% |

In the end, knowing how your Fixed Deposit grows is as important as the interest rate. Your final return depends on several things: the interest rate, how long you invest, how often you get paid (monthly or at maturity), and the required tax deduction (TDS) in Nepal.

Calculating interest by hand is a good way to learn and check your bank’s maturity amount, but it takes time and can lead to mistakes.

For faster, more accurate, and tax-adjusted results, use an online FD calculator in Nepal. These tools make it easy to compare returns for different time periods and banks, so you can make the most of your money.

Want to see how much your money will grow? Skip the complex formulas and use Saral Banking Sewa’s Fixed Deposit Calculator for a full comparison of interest rates from different banks. Plan smart and save better!

In Nepal, FD interest is typically calculated using the simple interest formula (Principal × Rate × Time / 100) for tenures under a year. For longer tenures or specific schemes, banks often use quarterly compounding. Remember, a 6% Tax Deducted at Source (TDS) is applied to your total earnings before payout.

Yes, most commercial and development banks in Nepal compound interest on Fixed Deposits, usually on a quarterly basis (every 3 months). This means your earned interest is added back to the principal, helping your money grow faster compared to simple interest schemes.

If the interest rate is around 9.5% per annum, a Rs. 5 Lakh FD earns approximately Rs. 47,500 annually before tax. This translates to roughly Rs. 3,958 per month. However, after the mandatory 6% tax deduction, your net monthly hand-in-hand income will be slightly lower.

Manual calculation is tedious. The easiest way is to use the Fixed Deposit Calculator in Nepal by Saral Banking Sewa. Simply enter your deposit amount, tenure, and interest rate to instantly see your total maturity amount, tax deductions, and net profit without any math headaches.

Assuming an average interest rate of 10% per annum, a Rs. 10 Lakh deposit will generate a gross interest of Rs. 1,00,000 in one year. After deducting the 6% TDS (Rs. 6,000), your net earnings would be Rs. 94,000, bringing your total maturity amount to Rs. 10,94,000.

Interest rates change frequently based on liquidity. Generally, Finance Companies and Development Banks offer slightly higher rates (often 0.5% to 1% more) compared to Class 'A' Commercial Banks. To find the current highest earner, you must compare the latest published rates across all institutions.

You don’t need to visit every bank. You can easily compare the latest interest rates of all commercial and development banks side-by-side on Saral Banking Sewa’s General Fixed Deposit page. We update the data regularly so you always get the best deal for your investment.

Yes, the government of Nepal mandates a 6% Tax Deducted at Source (TDS) on all interest income for natural persons (individuals). Banks automatically deduct this amount from your accrued interest before crediting the remaining earnings to your account or adding it to your principal at maturity.

For wealth creation, yes. FDs offer significantly higher interest rates (often double) compared to savings accounts. However, savings accounts provide better liquidity for daily needs. A smart strategy is to keep emergency funds in savings and lock surplus money in FDs for maximum growth.