You’ve finally saved up some extra cash and want it to earn a safe return. Now comes the big question: should you lock it away for just a few months or for several years?

Fixed Deposits (FDs) are the go-to choice in Nepal because they offer a rare sense of calm in an unpredictable market. They are a true "cross-generational" favorite, trusted by everyone from students to retirees because the returns are guaranteed and the risk is almost zero.

Many people believe that longer-term investments always yield higher returns. However, interest rates can change, and locking in a long-term rate before they rise may cause you to miss better returns. In some cases, shorter-term rates can be more favorable. The important thing is to choose a timeframe that matches current market conditions.

This guide will help you understand the differences between short-term and long-term FDs. We'll look at current returns, which are around 3.62%, and provide a checklist to help you choose the best option for your situation. By the end, you'll feel confident about growing your money.

A Fixed Deposit is an agreement with your bank where you deposit a specific amount of money for a fixed period. In return, you earn a higher interest rate than in a regular savings account, making it a simple way to grow your money.

It's a simple process. You make a deposit, which can range from a few thousand to several lakhs, and select your term. Your interest rate is then locked in, ensuring that, regardless of market fluctuations, the bank must pay you the guaranteed return at the end. In Nepal, you can customize your FD based on when you think you will need the cash:

The key benefit of a fixed deposit (FD) is its stability. Unlike the stock market, which can fluctuate, an FD is considered risk-free and offers predictable returns. This makes it a great option for saving without worrying about market changes.

Think of a short-term FD as a "temporary parking spot" for your cash. If you have some extra money but know you’ll need it within a few months, perhaps for a wedding, business stock, or upcoming tuition fees, you don’t want it sitting inactive in a basic savings account where it earns very little.

Short-term FDs typically range from 3 months up to 12 months. It’s the perfect middle ground for people who want their money to work hard but aren't ready to say goodbye to it for years. You get a better interest rate than a regular account, but you still keep your financial flexibility. If a better opportunity comes along in six months, your money is back in your hands, along with the interest, ready for your next move.

Short-term FDs are designed for the regular saver who values freedom over everything else because your money is only locked away for a few months, you enjoy high liquidity, meaning your cash is back in your hands and ready to use much sooner.

While the interest rates are typically a bit lower than long-term options, you aren't "trapped" if the market changes; you stay flexible and are less affected by those big, long-term rate shifts. It’s the ideal choice if you want to keep your savings safe and productive without losing the ability to pivot when life happens.

Short-term FDs are perfect for life’s "in-between" moments, like when you’re saving for a vacation, keeping business cash flow balanced, or building a quick emergency fund. Since your money is only locked away for a few months, you aren't "trapped" if your situation changes.

The biggest advantage is the flexibility to reinvest. In the current market, interest rates can shift quickly. With a short-term commitment, you can move your funds into a higher-paying plan the moment your current one matures. It’s the ideal plan for anyone who wants to earn a reasonable return today while keeping their options wide open for tomorrow.

While short-term FD offers great flexibility, they aren’t always the perfect fit. A few trade-offs to keep in mind:

If a short-term FD is a temporary parking spot, a long-term FD is more like planting a tree. You set aside a lump sum of money today and let it grow undisturbed for a considerable period, typically 2 to 5 years or more. It is the greatest tool for wealth protection and long-term savings.

These deposits are perfect for those who want to build a secure future rather than seek quick returns. Whether you’re saving for your child’s education, planning to build a house, or preparing for retirement, a long-term fixed deposit (FD) helps your money grow over time. By saving for the long term, you gain peace of mind, knowing your financial foundation is stable and growing.

Long-term FDs are built for the patient saver who wants to maximize their earnings. The most obvious draw is the higher interest rate; banks generally pay you a premium for committing your money for a longer period. Because your rate is locked in for the entire tenure, you are protected from market dips, ensuring your returns stay high even if the economy cools down.

Beyond the rate, these deposits offer powerful compounding benefits, especially if you reinvest the interest, allowing your money to grow exponentially over time. It also acts as a "savings shield," encouraging disciplined saving by keeping your funds tucked away and out of reach for impulse spending. It’s the perfect way to turn today’s savings into a much larger nest egg for the future.

Choosing a long-term FD is like making a promise to your future self. Here is why it often makes the most sense for serious savers:

While the high returns of a long-term FD are tempting, they come with certain "rules of the game" that you need to be aware of:

Choosing the right FD isn’t just about picking the highest number you see; it’s about matching the bank’s timeline with your life’s timeline. To help you decide, here is a quick look at how they stack up side by side:

| Feature | Short Term FD (3 to 12 months) | Long-term FD ( 2 to 10 years) |

| Interest Rates | Generally Lower | Generally higher (premium for patience) |

| Liquidity | High: Money is back in your hands quickly | Low: Money is committed for years |

| Flexibility | High: Easy to reinvest if rates rise | Low: Locked into a set rate for the duration |

| Risk | High reinvestment risk (rates might drop) | High opportunity cost (rates might rise) |

| Compounding | Minimal impact over short cycles | High impact: Wealth grows significantly |

| Best use cases | Emergency funds, weddings, travel | Retirement, education, and house building |

The "better" option isn't always the one with the highest interest rate. It really comes down to your personal priorities:

At the end of the day, "better" is defined by your goals, not just the bank's chart. If you need that money for a business deal in six months, a 5-year FD, no matter how high the rate, is the wrong choice.

In the Nepalese market, the "better" return isn't just about the interest rate you see on the bank’s notice board; it’s about how that rate interacts with time and the economy.

Generally, long-term FDs provide higher overall returns. Banks in Nepal operate on a simple principle: they reward your dedication. By letting the bank use your money for 5 or 10 years, you provide them with stability, and in return, they offer a "premium" interest rate that is typically 1% to 2% higher than short-term options.

Over several years, this difference becomes huge. Thanks to the power of compounding, even a slightly higher rate on a long-term deposit can generate a much larger final payout than repeatedly opening short-term accounts.

It’s not always a one-sided race. There are specific scenarios where a short-term strategy can actually put more money in your pocket:

Sometimes, the best move for your money isn’t the one that locks it away for the longest time, but the one that keeps it within reach. A short-term FD is your best backer when flexibility is your top priority. You should consider going short-term in the following situations:

A long-term FD is the perfect choice when you want to stop worrying about market ups and downs and focus on building serious wealth. It is the strategy of choice for the "patient investor" who wants to secure their future today. You should opt for a long-term commitment in these scenarios:

If you’re still confused between choosing a short-term or long-term FD, there is a "pro" technique that gives you the best of both worlds: FD Laddering.

Instead of putting all your money into one plan, you split it into several FDs with different end dates. This creates a "ladder" of cash, so some money is always available while the rest continues to earn high interest.

Imagine you have NPR 3,00,000 to invest. Instead of putting it all into a single 3-year FD, you split it like this:

Laddering is the "Pro Move" for smart saving in Nepal. Here is why it works:

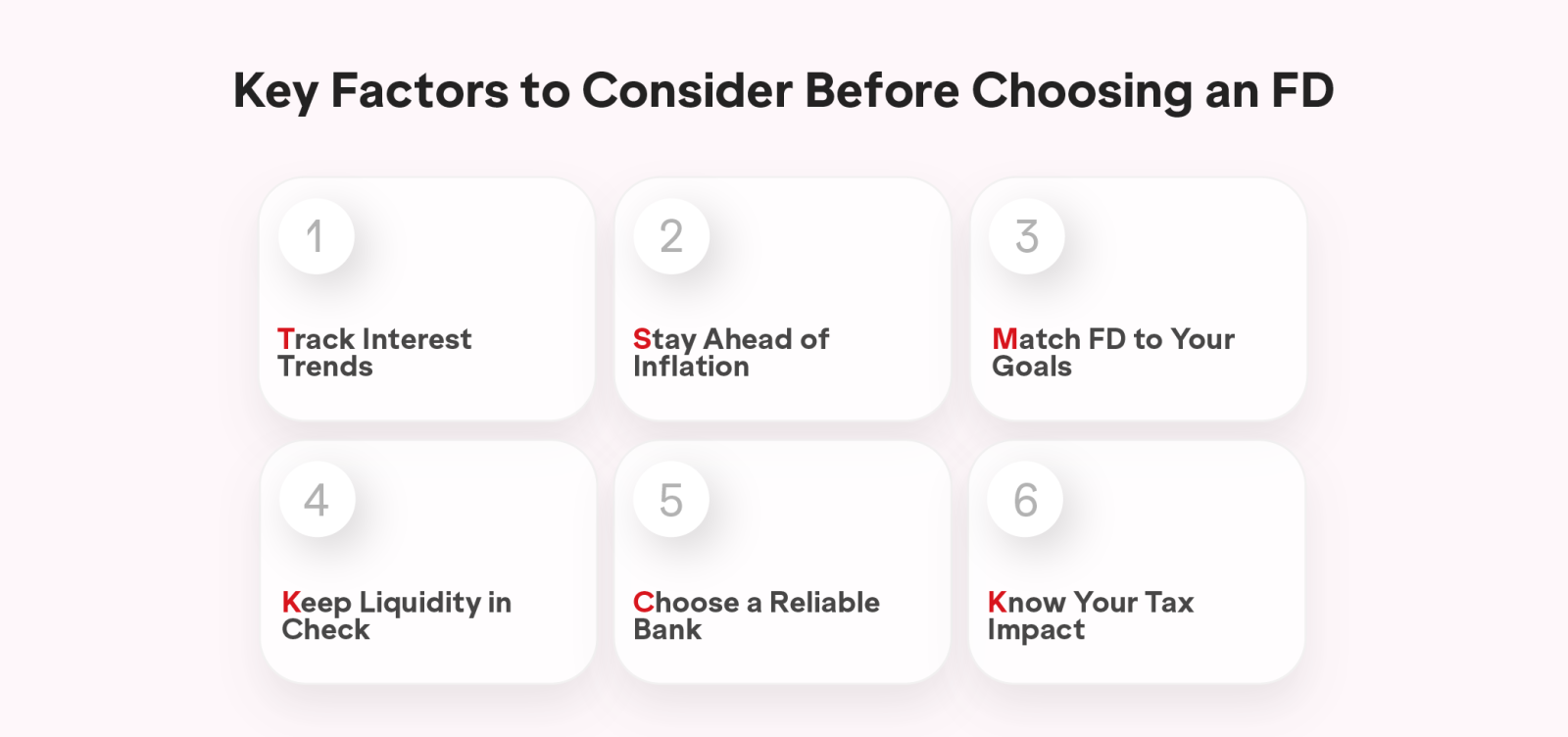

In Nepal’s growing financial market, picking an FD isn't just about finding the highest interest rate. To make your money truly work for you, keep these essentials in mind:

Every bank, from large commercial banks to smaller development banks, sets its own rates based on its funding needs. This means that simply walking into the nearest branch without checking other options could cost you thousands in lost interest over time.

Don’t waste your afternoon visiting different bank branches or scrolling through dozens of confusing websites. With Saral Banking Sewa, you can compare the latest FD rates across Nepal in one simple view. So, you can stop searching and start earning. Make the smartest move for your savings today, quickly, easily, and all in one place.

When it comes to picking a Fixed Deposit, there is no "one-size-fits-all" answer. The right choice depends entirely on your personal timeline and what you want your money to achieve. To wrap it up, here is the simple breakdown:

Remember, the smartest investors don't just pick a duration blindly; they assess their goals, compare the latest market rates, and use techniques like FD laddering to get the best of both worlds.

Don’t let your hard-earned money just sit there; make it grow. Stop guessing and start comparing at Saral Banking Sewa to find the best rates in Nepal today. Your future self will thank you.

Generally, long-term FDs offer higher returns because banks provide a premium interest rate for locking in your money for a longer period. However, short-term FDs can perform well if you reinvest them during a period where interest rates are rising.

In the Nepalese banking context, a short-term FD typically ranges from 3 months to 12 months. These are ideal for goals you expect to reach within a year.

Long-term FDs usually have a tenure of 2 to 5 years, and in some cases, up to 10 years or more.

Investing in FDs with "A" Class banks regulated by Nepal Rastra Bank is safe, with deposits up to NPR 5,00,000 insured by the DCGF.

Yes, most banks allow "premature withdrawal," but it comes with a cost. You will typically face a penalty fee or receive a lower interest rate than originally promised.

No, rates vary significantly. Each bank sets its own rates based on its liquidity needs and NRB guidelines. Always compare rates before opening an account.

FD laddering is a process in which you split your investment across multiple FDs with different maturity dates (e.g., 1-year, 2-year, and 3-year). This ensures you have regular liquidity while still earning high long-term interest.

Yes. Choosing a short-term FD helps you avoid getting stuck at a lower rate. When your short-term FD matures, you can reinvest that money at the new, higher market rate.

The fastest and most reliable way is to use Saral Banking Sewa’s FD comparison tool. It allows you to see the latest rates from all Nepalese banks in one place, helping you make a smart, profit-driven choice in seconds.