Did you know that according to the Nepal Rastra Bank (NRB), our national financial literacy rate stands at only 58%? This means nearly half of the population is facing their finances without clear advice, often struggling to make ends meet by the end of the month.

In today’s economy, saving isn’t just a "good habit"; it’s a survival skill. Between the rising costs of rentals, the changing price of petrol, and the ever-increasing school fees for children, the traditional way of "saving what is left" simply isn't working anymore.

Whether you are a student managing a tight pocket-money budget, a corporate employee in a 9-to-5, or a head of a household, this guide is for you. We aren't just going to talk about cutting back on your daily Tea costs, but we are going to explore practical, modern strategies to reduce expenses and increase your income in the Nepalese context.

In our society, we have a common saying: Wealth that is saved protects you during a crisis ("Sanchay gareko dhanle sankat parda bachaucha"). But in the rush of daily life, balancing work, family, and social responsibilities, it’s easy to view saving as a secondary priority.

However, saving money in Nepal isn’t just about having a large bank balance; it’s about buying yourself peace of mind. Here is why building a savings habit is the smartest move you can make for your future.

Before you can save a single rupee, you need to know exactly where your money is coming from and, more importantly, where it is going. Think of your finances like a water tank: you can’t fill it up if you don’t know how much water is flowing in and where the leaks are.

Many of us depend on a single monthly salary, but in today’s "side-hustle" economy, your income might be more diverse than you think. Tracking isn't just for big businesses; it’s for anyone who wants to take control of their life.

Tracking your income helps you understand your financial strength, while tracking expenses reveals where your money is leaking. Many people in Nepal feel their money vanishes by the second week of the month due to small, overlooked expenses like Tea, transport fares, or snacks. These unrecorded costs can lead to financial stress. To reduce this stress, it’s crucial to identify exactly where your money is going.

Budgeting is often seen as limiting your fun, but it's really just a spending plan. Think of it as a road map for your money, helping you track where it goes. With a budget, you can enjoy spending on things like clothes or dining out without worrying about your upcoming expenses. It gives you more freedom.

The 50/30/20 Rule

A great way to regain control of your finances is by following the 50/30/20 rule. This strategy splits your monthly take-home income into three clear "buckets" to ensure you're covering your present needs while securing your future:

If percentages feel too complicated, just use the Three-Box Method. Every time you get paid, visualize three boxes. Put money into the Needs box first, then move a set amount into the Savings box. Whatever is left in the Wants box is yours to spend guilt-free. The secret to success here is to move the "Savings" money before you start spending on "Wants."

If your monthly take-home salary is NPR 30,000, start by setting aside NPR 15,000-18,000 for essentials like rent and groceries. Next, save NPR 3,000 to NPR 5,000 in a separate account for emergencies. This leaves you with about NPR 7,000 to NPR 10,000 for fun activities like dining out or shopping.

By following this simple structure, you ensure that your rent is always paid and that you are building your future, all while still enjoying your daily life in Nepal.

A common myth in personal finance is that you need a high salary to save money. In truth, saving isn’t just about how much you make; it’s about how you manage what you have. Smart management of even a modest income can lead to real savings over time. The key is to create a system that works for you, instead of just working to pay bills.

If you want to move beyond "keeping cash under the mattress," a proper bank account is your foundation. It’s the safest and most systematic way to ensure your money grows rather than just sitting idle.

Currently, interest rates for standard savings accounts in Nepal generally range from 2.75% to 3.00%, while specialized accounts (such as Remittance Savings) can reach up to 4.00%. Always compare your options to secure your money; work as hard as possible. You can compare different savings account types and rates in Nepal via Saral Banking Sewa to find the best fit for your goals.

One of the most effective tricks is to have two accounts: one for your daily expenses (where your salary lands) and another for savings. By moving your "future fund" to a different account, you reduce the urge to spend it on an unnecessary purchase at the mall.

Take the "effort" out of saving. Most Nepali banks now allow you to set up a standing instruction or a recurring deposit (RD). This automatically moves a fixed amount, say Rs. 2,000, from your salary account to your savings or FD account every month. If you don't see the money in your main account, you won't miss it!

Tools like eSewa, Khalti, and your bank’s mobile app are for more than just paying bills. Use them to track your balance in real-time. Seeing your savings grow on your screen every week provides a "hit" of motivation that keeps you on track. Plus, digital statements make it incredibly easy to review your spending habits at the end of the month without visiting a branch.

In the world of personal finance, some of the most reliable tools for the average Nepali saver are Fixed Deposits (FD) and Recurring Deposits (RD). While the stock market can be a rollercoaster, these bank-backed instruments offer a "set it and forget it" approach that is perfect for those who want safety combined with guaranteed returns.

A recurring deposit (RD) is ideal for salaried individuals with a steady income. You can easily set aside a small, fixed amount each month, such as Rs. 2,000 or Rs. 5,000, for a set period. Many banks in Nepal now offer automation, allowing your deposits to be made on payday. After two years, you’ll find a nice lump sum waiting for you, along with interest.

If you have a lump sum of money from a bonus, gift, or matured insurance policy, consider putting it in a fixed deposit (FD) instead of a regular savings account. FDs typically offer higher interest rates, ranging from 3% to 4.25% for 1-year terms, compared to the 2.75% to 3% of regular accounts. Since these deposits are regulated by the Nepal Rastra Bank (NRB), they are a low-risk option for growing your wealth in Nepal.

If you're saving for something like a bike, college tuition, or a wedding, RD and FD can help you manage your money. They keep your funds safe from impulsive spending while remaining accessible when you need them. To avoid locking all your money in a long-term FD, consider FD Laddering: divide your funds into three smaller FDs with different maturity dates (e.g., 6 months, 1 year, and 2 years). This way, you get some cash back sooner while the rest earns interest.

Once you’ve mastered the habit of saving in a bank account, the next step is to make your money grow. While a savings account is great for storage, it often barely keeps up with inflation. If you want to build real wealth over time, you need to look toward the stock market, but you don’t have to be a professional trader to do it.

Small Monthly Investments

A Systematic Investment Plan (SIP) is a beginner-friendly way to invest in the stock market, allowing you to contribute a fixed amount, starting at Rs. 1,000 per month, into an open-ended mutual fund. Professional fund managers use your money to buy fund "units," benefiting from "rupee cost averaging," which helps balance out investment costs and ease trading stress.

Long-Term Wealth Building

The true advantage of a SIP lies in its long-term potential, driven by compounding returns. Over time, the returns you earn can grow your wealth if left untouched, making it ideal for long-term goals like education, retirement, or buying a home. Think of it like raising a pipal tree: patience and discipline lead to lasting security.

Better Than Keeping Money Idle

While traditional savings accounts and FDs offer safety, they often fall behind inflation, reducing your money’s buying power. Whereas, mutual funds invest in a diverse mix of assets and can deliver higher long-term returns while spreading risk across various companies, making them a more effective wealth-building tool.

Many of us think of saving as something to do at the end of the month with leftover cash. But with online sales and food delivery, that leftover money often doesn’t exist. To build true wealth in Nepal, it’s important to treat savings like a crucial monthly bill.

Whether it’s a sudden medical bill for a family member, a period of job instability, or an urgent repair for your home or motorbike, these "uninvited" expenses often strike when we are least prepared. An emergency fund is your financial "insurance policy"; it ensures that a temporary crisis doesn’t turn into a permanent debt trap.

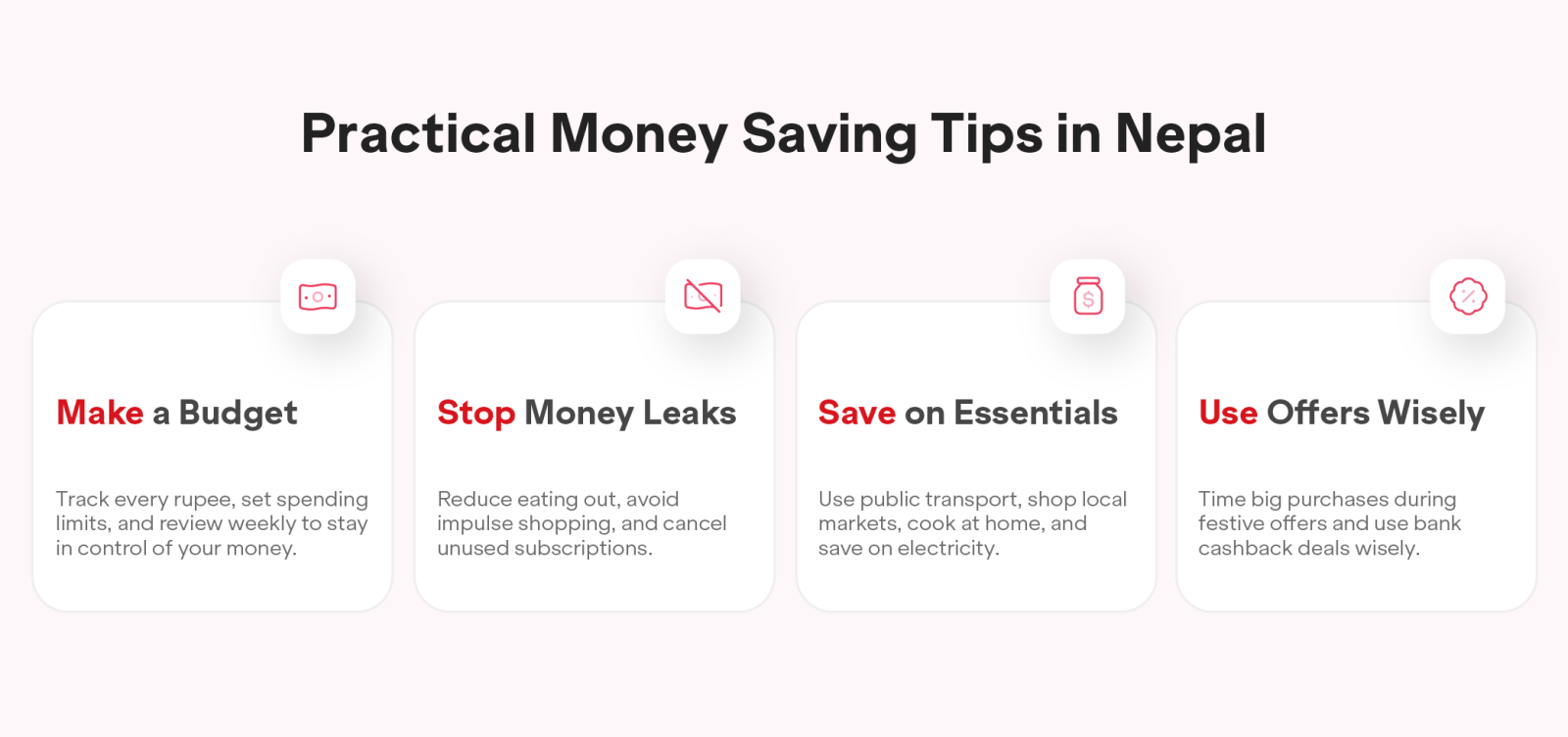

Knowing why we should save is the first step, but the real magic happens in the how. In Nepal, where the cost of living, especially for items like fuel and imported goods, can change overnight, having a practical day-to-day system is essential. It’s not about being cheap; it’s about being intentional.

Think of a budget not as a cage that keeps you in, but as a tool that lets you see exactly where your hard-earned money is going. Without a budget, your income is like water poured onto sand; it disappears before you can even track the flow.

In the age of social media, it is very easy to feel like we need to live a certain lifestyle to keep up with our friends. However, those "small" daily habits are often the biggest reason why many of us feel broke by the 20th of the month. Saving money doesn’t mean you stop enjoying life; it just means you stop letting your money leak out of your pocket unnoticed.

Between irregular petrol prices and the convenience of modern supermarkets, it is easy to overspend without realizing it. However, with a few traditional habits and a bit of planning, you can significantly lower your daily cost of living without compromising your quality of life.

There is a saying that "money saved is money earned," and there is no better time to apply this than during our major festive seasons. However, the trick is to use discounts to buy what you need, rather than letting a "sale" trick you into spending money you don't have.

While cutting expenses is a good start, there's only so much you can cut. On the other hand, you can always increase your income. In Nepal's economy, depending on a single paycheck is risky. Diversifying your income is important, not just for the wealthy, and it can help you achieve your goals faster.

The most successful financial managers in Nepal are those who view their time as an asset. If you find that your monthly savings aren't growing despite your best efforts to cut costs, it’s time to shift your focus from "saving pennies" to "earning rupees."

In the past, managing money meant keeping a heavy "khaata" or collecting a pile of paper receipts that usually ended up in the trash. Today, your smartphone is the most powerful financial tool you own. Managing money becomes significantly easier and even fun when you let digital tools do the heavy lifting for you.

Expense Tracking Apps: Apps like Monefy and Wallet help you see where your money goes each month. By categorizing expenses (like Food, Travel, and Rent) and creating pie charts, these apps provide a visual representation of your spending habits, offering a helpful reality check.

We often spend 15 to 20 years in schools and colleges learning how to work for money, but we rarely spend even a few hours learning how to make money work for us. The truth is, financial knowledge is a long-term investment that pays lifelong returns. You don't need to be a math genius or a banker to be "money smart"; you just need to be curious.

We often blame a "low salary" for our financial struggles, but the truth is that many financial problems in Nepal stem from poor habits rather than the size of our paycheck. Even with a high income, many people find themselves in a "debt trap" because they haven't learned the basics of money management. By avoiding these common pitfalls, you can ensure that your hard-earned money stays with you and grows over time.

Building financial security in Nepal can be challenging, especially with rising living costs. However, saving money is possible with discipline and smart planning. You don’t need a high salary to start; managing your earnings wisely is key.

Achieving a stress-free life takes time and consistent effort. Focus on tracking your expenses, skipping unnecessary purchases, and saving regularly, whether it’s Rs. 500 or Rs. 5,000. What matters most is developing the habit of saving.

Don’t wait for the “perfect time” or a higher salary to start saving. Begin today, wherever you are. Every financial success story starts with a small step and the determination to stay committed. By taking control of your finances now, you're not just preparing for the future; you're creating a more stable life for yourself and your family.

Your journey to financial freedom starts with the very next rupee you spend. Make it count.

The best way to save money in Nepal is to "save first, spend later" by automating your savings. Set a standing instruction to transfer a part of your salary to an RD or a separate account immediately. Additionally, choose public transport over taxis and local markets over expensive markets.

Yes, personal financial management is helpful even with low income. It helps you track spending, control expenses, and save small amounts regularly, making it easier to avoid debt and improve financial stability over time.

The best way to start managing your personal finance is by tracking your expenses for 30 days using a notebook or apps like eSewa. Once you see where your money goes, apply the 50/30/20 rule to prioritize needs, control wants, and build a consistent saving habit.

Aim for 10% to 20% of your take-home pay. If that’s too high, start with even 5%. The goal is to build the discipline of saving something every month, regardless of the amount.

You can use a savings account for emergency cash you might need instantly. Whereas, choose an Fixed Deposit for money you don't need for several months, as it offers quite high interest rates (often around 3.00% to 4.50%).

Students should use "Student Savings Accounts" for better rates and no minimum balance. Save by using your student ID for transport discounts, carrying a home-cooked tiffin, and buying second-hand books.

The best way to invest money in Nepal depends on your goals, but common options include fixed deposits, mutual funds, real estate, and government bonds. For beginners, low-risk options like savings and fixed deposits are usually safer and more stable.

A 50-30-20 rule of money is a simple budget split method where you seperate 50% for Needs (rent, food), 30% for Wants (entertainment, dining), and 20% for Savings and debt repayment.

A Recurring Deposit is a savings scheme where you deposit a fixed amount every month for a set time. It helps build disciplined savings and earns interest safely over time.

Rates change frequently based on market conditions. To find the best returns for your money right now, you can compare fixed deposit rates in Nepal here in Saral Banking Sewa.