So, you have finally found the car you want. Maybe it's that sleek electric vehicle you've been eyeing, or a reliable family SUV. The excitement is real, but then comes the paperwork.

If you've ever walked into a bank with what you thought was everything, only to be told, "Please bring one more document," you know how frustrating that cycle can be. The good news? That back-and-forth is almost always avoidable.

Most auto loans in Nepal aren't rejected because of low income. They're delayed or denied because of missing, outdated, or incorrect documents. This guide gives you the complete checklist, so you walk in prepared and walk out approved.

Before we get into document requirements, let's make sure you qualify. Here's what most Nepali banks look for:

Who can apply?

Age requirements:

Income rule (the 50% rule): This is the big one. Your total monthly EMI payments, including this new loan, must not exceed 50% of your gross monthly income. In certain cases, for higher income brackets, banks may allow up to 70%.

For example, if you earn NPR 80,000 per month, your total EMIs across all loans cannot exceed NPR 40,000.

If you're a first-time borrower, don't worry too much about this. Just make sure your salary slips are clean and up to date; that's what matters most at the start.

Check whether you are eligible for a loan or not by knowing how much loan you can take with the Loan Eligibility Checker tool.

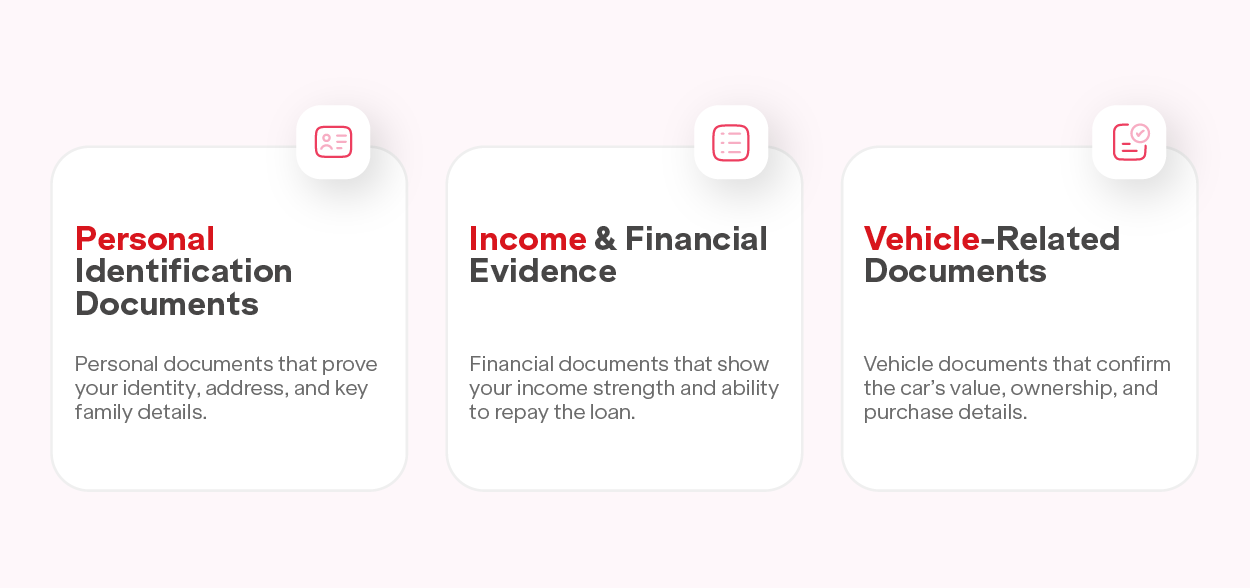

Think of your loan file in three buckets: who you are, how much you earn, and what you're buying. Here's exactly what goes in each.

These prove your identity and where you live. Banks are strict about this requirement; blurry photocopies or expired documents will slow things down immediately.

| Document | Details |

| Citizenship Certificate | Self-attested, clear copies of both the applicant and the guarantor |

| Passport Size Photos | 3 copies each for borrower and guarantor |

| PAN Certificate | Mandatory for all auto loans; strictly required for loans above NPR 25 lakhs |

| Location Map | Hand-drawn or digital map of your home AND office address |

| Relationship Certificate | Required if you're including family members' income in your application |

| Marriage Certificate | Needed if applying jointly with a spouse |

| Rental Agreement / Land Ownership Docs | Proof of your current residence address |

What you should do: You should self-attest every photocopy yourself, sign across the copy, and write "Self-attested." Don't ask someone else to do it.

This section determines how much loan you get. Banks are most careful here, so make sure everything in the loan documents is current and consistent.

If you work a regular job and receive a fixed monthly salary, you'll need:

If you are running your own business, you will need a few more required documents, but it's all standard:

Many Nepali families rely on income from a family member working overseas. Banks do accept this, but the documentation needs to be solid:

What you should know: Cash remittances sent through informal channels (hundi) are not accepted. All transfers must go through official banking channels.

Once your personal and financial documents are ready, the bank also needs to verify what you're actually buying

| Documents | When it's needed |

| Pro-forma Invoice | Always required. It is the official quotation from the authorised dealer (e.g., Tata, Hyundai, BYD) |

| Blue Book Copy | Required for used/second-hand vehicle financing |

| Valuation Report | For used vehicles only. It must be from a bank-authorized valuator |

| VAT Bill / Purchase Agreement | Confirms the vehicle price for new cars |

| Insurance Quote | Some banks ask for this upfront as part of the file |

Here's something many borrowers don't realise: what you're buying changes what you need to submit and how much the bank will finance.

Nepal's banking sector has been actively encouraging EV adoption. In 2026, most banks offer preferential treatment for electric vehicles:

Traditional ICE vehicles are financed on stricter terms:

You've handed in your complete file. What now? Here's the typical process:

These small moves can save days, sometimes weeks, off your approval timeline:

Getting an auto loan in Nepal in 2026 isn't complicated, but it is detail-oriented. The banks aren't trying to make your life difficult. They just need to trust that you'll repay what you borrow.

The difference between a loan that's approved in 3 days and one stuck in "pending" for 3 weeks is almost always the completeness of your required documents for an auto loan. Use the checklist in this car loan document requirements guide, double-check every document, and you'll be handing over your down payment before you know it.

Once your documents are sorted, the next step is finding the right bank, one that offers the lowest interest rate and the most reasonable processing fee. Instead of visiting branch after branch across Nepal, collecting brochures and rate sheets, use the Saral Banking Sewa Auto Loan Interest Rate Comparison tool to compare the latest auto loan rates from all major Nepali banks in one place.

Save your energy for the drive home. Let the Saral Banking Sewa’s interest comparison tool do the bank-hunting for you.

At a minimum, you need your Citizenship Certificate, PAN card, passport-size photos, 6-month bank statement, salary certificate or income proof, and a pro-forma invoice from the vehicle dealer. Having all six ready gets your application moving immediately.

Yes. A PAN card is mandatory for all auto loans in Nepal, regardless of vehicle type. It becomes strictly required for loans above NPR 5 million. Bring both the original and a self-attested photocopy to your bank visit.

It's difficult. Banks require a bank statement showing regular salary credits. If you're paid in cash, ask your employer to start depositing your salary into your account at least 6 months before you apply.

For used vehicles, you additionally need the original Blue Book (ownership certificate), a Valuation Report from a bank-authorised valuator, and the seller's ownership transfer documents. Some banks may also request a vehicle inspection report.

Yes, absolutely. You can add your spouse as a co-borrower. Their income is then combined with yours, increasing your total eligible loan amount. You'll need their citizenship certificate, proof of income, and passport-size photos.

Generally, no. Auto loans in Nepal are secured against the vehicle itself; the bank marks a lien on the Blue Book. A Lalpurja is not typically required unless you're applying for a significantly larger loan amount.

Freelancers should submit 12 months of bank statements showing regular income deposits, foreign remittance receipts, contracts or invoices from clients, and a PAN certificate.

Visit any authorised dealership and request a Pro-forma Invoice for your chosen vehicle. It's an official price quotation, not a binding purchase contract. You're not committed to buying; it simply tells the bank exactly what you're financing.

Yes! Saral Banking Sewa can help you apply for an auto loan in Nepal. We help you compare interest rates from all major banks, prepare your documents, and connect you with the right lender, saving you time and unnecessary bank visits.