A low credit score doesn’t always mean your loan application will be rejected. In Nepal, banks and financial institutions look beyond a single number when deciding whether to approve a loan. While your credit score has become an increasingly important indicator of your borrowing history and repayment behavior, it is only one part of your overall financial profile.

Many borrowers assume that a low credit score automatically leads to loan rejection. In reality, lenders also assess factors such as your income, employment stability, existing loan obligations, repayment capacity, and the purpose of the loan before making a decision. A strong financial profile in these areas can sometimes improve your chances, even if your credit score is less than ideal.

Understanding how lenders evaluate loan applications can help you prepare better, avoid common mistakes, and make informed financial decisions.

In this blog, we will explain whether you can get a loan with a low credit score in Nepal, the factors banks consider during the approval process, and the practical steps you can take to improve your chances of securing a loan.

A credit score is a numerical indicator of your creditworthiness, based on your borrowing and repayment history. It forms part of your overall credit profile and helps banks and financial institutions assess your repayment behavior and the likelihood of repaying a loan on time.

A good credit score usually reflects responsible financial habits, such as paying loan installments on time and managing debt well. Whereas a poor credit history may include frequent late payments or loan defaults, which can make lenders more cautious.

For example, someone who regularly pays their loan installments on time is likely to have a stronger credit profile than someone who regularly misses payments. That’s why maintaining a good repayment record can improve your chances of getting approved for a loan.

When you apply for a loan, banks and financial institutions want to ensure that you can repay the borrowed amount on time. To reduce lending risk, they carefully review your credit history, which reflects how you have managed your past and current credit obligations.

Lenders consider several factors, including your previous loan repayment record, whether you have missed any EMI payments, any history of loan defaults, and your credit card payment behavior. They also assess your existing outstanding loans to understand your current debt burden and repayment capacity.

A history of timely repayments shows financial responsibility and can improve your chances of loan approval. On the other hand, frequent missed payments, loan defaults, or high outstanding debt may make lenders more cautious. While your credit history is an important factor, it is assessed alongside your income, employment and overall financial profile before a lending decision is made.

Yes, it is possible to get a loan with a low credit score in Nepal. However, approval depends on several financial factors, not just your credit score. While a low score may reduce your chances, it does not automatically mean your loan application will be rejected.

Lenders look at your overall financial profile before making a decision. You may still qualify for a loan if you have a stable monthly income, a long and consistent employment history, or are applying for a smaller loan amount. Offering strong collateral, applying with a guarantor or co-applicant, or showing improved recent financial behavior can also strengthen your application.

It’s important to remember that every bank and financial institution has its own lending policies and risk tolerance. Some lenders may be more flexible than others, depending on the type of loan and your overall ability to repay. That’s why a low credit score should be seen as one factor in the approval process, not the only one.

A credit score is only one part of the loan approval process. Banks and financial institutions in Nepal also evaluate your income, employment, existing debt, collateral, and the purpose of the loan to determine whether you can comfortably repay the borrowed amount.

Banks assess your regular source of income, whether it comes from a salary, business, rental property, or other reliable earnings. A stable, regular monthly income is often more important than occasional high earnings because it demonstrates you can make timely loan repayments.

Lenders also consider how stable your employment is. Government employees, private-sector workers, self-employed professionals, and business owners can all qualify for loans, but a longer, more consistent work history generally gives banks greater confidence in your ability to repay.

Your current financial obligations, such as EMIs, credit card balances, personal loans and business loans, affect your loan eligibility. Banks generally assess your debt-to-income ratio or repayment capacity to see how much of your monthly income is already used to repay debt. A lower DIT usually improves your chances of loan approval.

For secured loans, collateral helps reduce the lender’s risk. In Nepal, assets such as land, buildings, fixed deposits, or vehicles may be accepted as collateral, depending on the loan type. Unsecured loans, which don’t require collateral, are usually approved based on higher income and credit profiles.

Banks also evaluate why you need the loan. Whether it’s for buying a home, higher education, medical expenses, business expansion or purchasing a vehicle, the loan purpose helps lenders determine your eligibility and choose the most suitable loan product.

Even with a low credit score, you may still qualify for certain types of loans. Since every lender has different approval criteria, choosing the right loan product can improve your chances.

Secured loans are backed by collateral such as property or fixed deposits. Because the collateral reduces the lender’s risk, these loans are often easier to qualify for than unsecured loans.

Some banks may offer personal loans to salaried individual with a stable income and a strong repayment capacity, even if their credit score is lower than ideal. Other financial factors are considered before approval.

Since home loans are secured by the property being purchased, they may have a better chance of approval than unsecured loans. Lenders also assess your income, repayment capacity, and property value. Learn more about home loans by clicking here.

For business loans, lenders look beyond your credit score. They review your business performance, cash flow, financial statements, and revenue to determine whether your business can comfortably repay the loan.

A loan against a fixed deposit is often one of the easiest options because the FD serves as security. As a result, these loans usually have a faster approval process and may be available even to borrowers with lower credit scores.

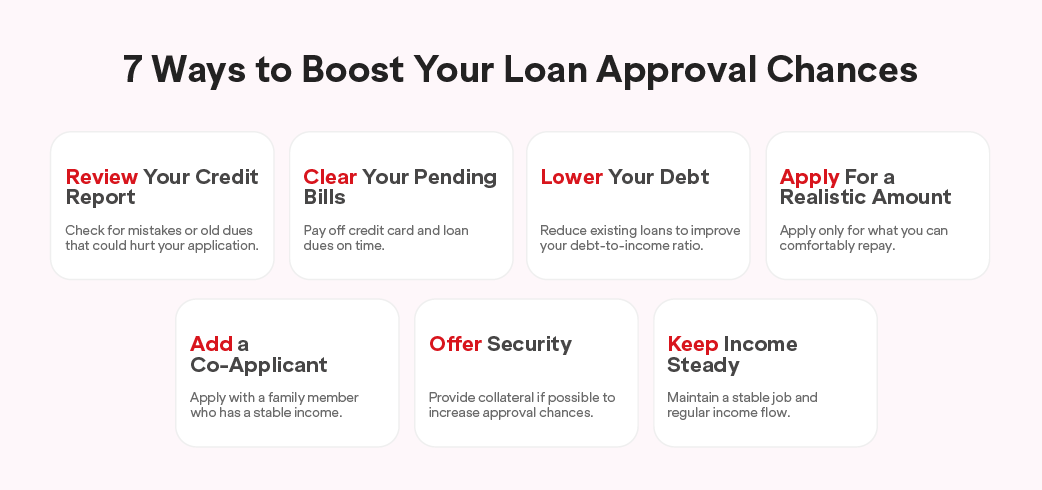

If you have a low credit score, there are several steps you can take to strengthen your loan application. Improving your overall financial profile can increase your chances of getting approved, even if your credit score isn’t perfect.

Review your credit history before applying for a loan to identify any errors or overdue payments. Understanding your credit profile also helps you know where you need to improve. You can also read our guide on “How Credit Score Affects Loan Approval”

Clear pending credit card bills, loan EMIs and other overdue balances whenever possible. Timely repayments demonstrate financial responsibility and improve your overall credit profile.

Lowering your existing debt makes it easier for banks to see that you can afford another loan. Paying off smaller loans first and avoiding unnecessary borrowing can improve your debt-to-income ratio.

Request a loan amount that matches your income and repayment capacity. Applying for an amount you can comfortably repay improves your chances of approval.

Applying with a spouse or family member who has a stable income and a strong financial profile can increase your loan eligibility and give lenders more confidence.

If possible, apply for a secured loan by offering eligible collateral. Since collateral reduces the lender’s risk, secured loans are often easier to obtain.

A stable income reassures lenders that you can make irregular repayments. Avoid changing jobs just before applying for a loan, and maintain a consistent salary or income deposit to strengthen your application.

A loan application is rarely rejected because of a single factor. In most cases, banks and financial institutions assess multiple aspects of your overall financial profile before deciding whether to approve or reject your application.

Missing loan EMIs, defaulting on previous loans, or making frequent late payments can signal a higher risk of repayment and negatively affect your loan application.

If you already have several loans or large credit obligations, banks may determine that taking on additional debt could be difficult to manage.

Your income should be enough to cover both your daily expenses and loan repayments. If your earnings are too low for the requested loan amount, approval may be less likely.

Missing or incorrect documents can delay the verification process and may lead to your loan application being rejected. Always ensure your documents are complete and up to date.

Frequent job changes or an inconsistent source of income may make lenders uncertain about your future ability to repay.

Submitting loan applications to several banks within a short period can indicate financial stress and may reduce your chances of approval. It’s better to apply after choosing the lender and loan product that best fit your needs.

A loan rejection doesn’t mean you won’t qualify in the future. By improving your financial profile and choosing the right borrowing option, you can increase your chances of approval the next time you apply.

Pay your EMIs and credit card bill on time, clear overdue balances, and maintain a repayment record before submitting a new loan application.

Applying for a lower loan amount that better matches your income and repayment capacity can improve your chances of approval.

If you have eligible assets such as property or a fixed deposit, consider applying for a secured loan. Collateral reduces the lender’s risk and may make approval easier.

Provide complete and accurate proof of income, such as salary slips, bank statements, tax records, or business financial documents, to demonstrate your ability to repay.

Maintaining a healthy banking relationship through regular transactions, savings, and responsible use of financial products can help build trust with your bank over time.

A low credit score doesn’t guarantee rejection of a loan application, as banks in Nepal also consider your overall financial health, including income, employment stability, existing debt, repayment capacity, and collateral.

To improve your chances of approval, pay bills and EMIs on time, reduce debt, maintain a stable income, and submit accurate documentation. These actions strengthen your application and promote a healthier financial profile.

When borrowing, compare loan options carefully and select one that aligns with your repayment capacity, rather than opting for the highest amount available. Responsible borrowing helps avoid financial stress and maintains a positive credit history.

Before applying for a loan, it's worth checking your credit score to understand how lenders may view your application. You can use Saral Banking Sewa's Credit Score Checker to review your credit profile and identify any issues that may affect your eligibility. It's a simple first step that can help you make informed borrowing decisions and apply with greater confidence.

Yes, it is possible. A low credit score does not automatically disqualify you from getting a loan. Banks also consider your income, employment, existing debt, repayment capacity, collateral, and other financial factors before deciding whether to approve your application.

No. A low credit score is only one part of the lending decision. If you have a stable income, manageable debt, strong collateral, or a guarantor, you may still qualify. Every bank has its own lending policies and risk assessment process.

Banks also evaluate your monthly income, employment stability, repayment capacity, existing loans, debt-to-income ratio, collateral, loan purpose, and supporting documents. These factors help lenders determine whether you can comfortably repay the loan on time.

Yes. Collateral reduces the lender's financial risk by serving as security for the loan. As a result, secured loans are more likely to be approved than unsecured loans, especially for borrowers with lower credit scores.

Yes, they can. Banks usually review business income, cash flow, financial statements, and repayment capacity. If the business is financially stable and generates consistent income, a self-employed borrower may still qualify despite having a lower credit score.

Improving a credit profile takes time and depends on your financial habits. Paying EMIs and credit card bills on time, reducing debt, and avoiding missed payments consistently over several months can gradually strengthen your credit profile.

Yes, paying off existing loans or reducing outstanding balances lowers your debt-to-income ratio. This shows lenders that you have a greater capacity to repay a new loan and can improve your chances of approval.

In many cases, yes. Since secured loans are backed by collateral, they involve less risk for lenders. This often makes approval easier than with unsecured loans, which rely mainly on your income, repayment history, and credit profile.

You can check your credit score through a trusted credit reporting service or a financial platform that offers credit score checks. Reviewing your credit profile before applying helps you identify any issues and prepare a stronger loan application.

It is generally better to avoid submitting several loan applications at once. Instead, compare loan options, choose the lender that best suits your needs, and apply only after ensuring your financial profile is ready.

Start by understanding why your application was declined. Then improve your financial profile by paying outstanding dues, reducing debt, strengthening your income documentation, or considering a secure loan before applying again.