Buying your first property is a big step toward achieving your individual financial goals. It may seem like there is a lot involved when it comes to securing a first mortgage home loan in Nepal. You are not alone; most people who apply for their first home loan in Nepal experience the same type of anxiety that you are feeling.

This is why we wrote this helpful guide. We believe it will give first-time homebuyers a full understanding of the entire process of acquiring a home loan in Nepal from start to finish. This guide will help first-time homebuyers who want to purchase a house in Nepal and need a loan. The guide is intended for all types of first-time homebuyers, whether salaried employees, self-employed, or business owners.

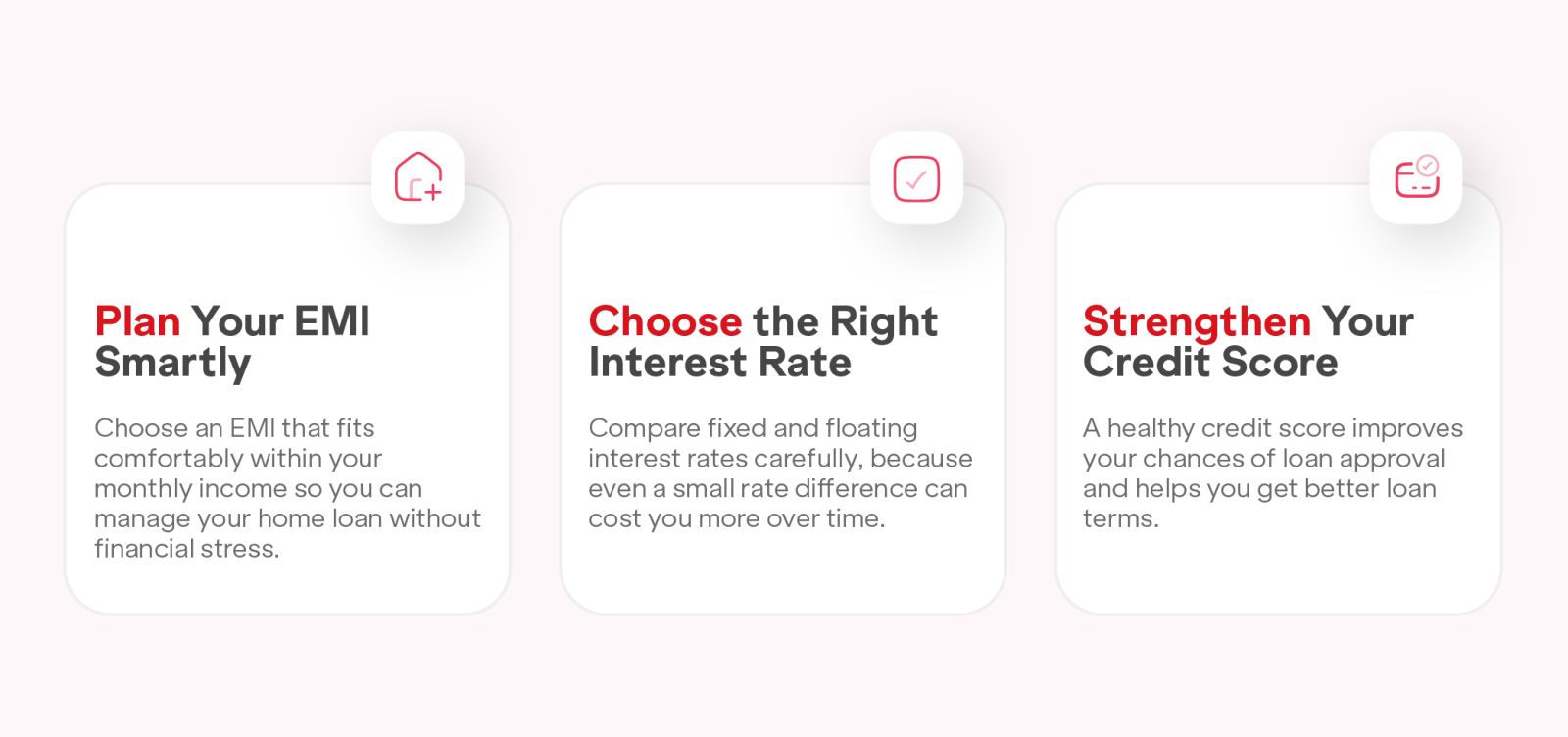

Before submitting a home loan application, it is important to conduct a thorough assessment of your financial capacity. You should calculate your EMI first. The Equated Monthly Installment (EMI) represents the fixed amount you will pay to your lender each month throughout the loan tenure.

Financial experts recommend that your EMI should ideally constitute between 30% and 40% of your gross monthly income. If your EMi is higher than 30% to 40% of your monthly income, it would be hard for you to maintain your essential expenses, such as daily living costs, utility bills, education expenses, and emergency savings.

For example, if your monthly income is NPR 80,000, your EMI should ideally range between NPR 24,000 and NPR 32,000. If you exceed the 30% to 40% threshold, it may create financial strain and compromise your ability to manage other important financial obligations.

It is advisable to use reliable EMI calculators to calculate your monthly EMI, like Saral Banking Sewa’s EMI calculator tool. Get instant and accurate EMI details and make your loan process easier.

Interest rates decide how much extra you'll pay over the years. Interest rates constitute a critical factor in determining the total cost of your home loan over its entire tenure. Even minor differences in interest rates can result in a substantial change in the loan payment amount. In Nepal, home loans typically feature two types of interest rate structures: fixed rates and floating rates.

The difference between interest rates may appear small at the beginning, but over a 20 or 25-year loan period, even a 0.5% variation can translate into differences of several lakhs of rupees in total interest paid.

So, to avoid paying a huge amount in interest, compare different banks before choosing. Don't just go with the first offer. Use tools like Saral Banking Sewa's home loan interest rates comparison to compare and see all your options in one place.

Think of your credit score as your financial report card. Your credit score serves as a quantitative representation of your creditworthiness and financial responsibility. Financial institutions in Nepal review credit scores maintained by the Credit Information Bureau to assess an applicant's repayment history and financial behavior.

A high credit score indicates consistent repayment behavior, responsible credit utilization, and low default risk. Having a high credit score helps in better loan approval chances and more favorable interest rates.

Similarly, a low credit score may result in loan rejection or higher interest rates since lenders perceive greater risk in extending credit to applicants with poor credit histories. In Nepal, the Credit Information Bureau keeps track of your credit history.

Therefore, before submitting your home loan application, it is advisable to obtain your credit report and review it for accuracy. Before you apply anywhere, check your credit score using Saral Banking Sewa's Credit Assessment.

If your credit score requires improvement, consider taking corrective measures such as clearing outstanding debts, paying credit card balances in full, and ensuring timely payment of all bills and existing loan installments.

The first step in the home loan process involves establishing a realistic budget based on your current financial situation, savings, and income level. Consider the type of property that best suits your needs and budget. You should decide whether you need independent houses that typically offer more space and privacy or apartments in multi-unit buildings.

An important consideration during this phase is to borrow only the amount you genuinely need, rather than the maximum amount a bank is willing to offer. Financial institutions may approve larger loan amounts based on your income, but accepting excessive borrowing can lead to long-term financial stress.

Conducting thorough research and comparison of loan products offered by different financial institutions is essential for securing optimal loan terms. Different banks in Nepal offer different interest rates, loan tenures, processing fees, and prepayment terms. These differences can have significant financial implications over the loan period.

Key factors to compare:

Rather than visiting each bank individually, which can be time-consuming and inefficient, you can use comprehensive comparison platforms such as Saral Banking Sewa to evaluate home loan offerings from multiple Nepali banks.

Each bank has its specific eligibility criteria that applicants must meet to qualify for home loan approval. Here are some of the important requirements before applying for a home loan.

Verifying your eligibility before submitting an application is crucial because applications that do not meet basic requirements will be rejected. Multiple loan rejections can negatively impact your credit score. Therefore, it is important to review each bank's specific eligibility criteria carefully and ensure you meet all requirements before applying.

Proper documentation is fundamental to a smooth loan application process in Nepal. Gathering all required documents before initiating your application can significantly reduce processing time and prevent delays.

Standard documentation requirements typically include:

Missing even one document can delay approval by several weeks. Therefore, to ensure you have all the necessary documents, consult the specific requirements of your chosen bank.

Saral Banking Sewa provides detailed information about documentation requirements for various banks and helps you to apply for your home loan smoothly.

Once you have completed preparing your documents, you can proceed with submitting your home loan application. Most banks in Nepal now offer both online and in-person application options. Online applications provide convenience and time efficiency, which helps you to complete the process from your home or office.

Also, in-person applications at bank branches help in direct interaction with loan officers, providing opportunities to ask questions and receive immediate clarification on any concerns. Regardless of the application method you choose, accuracy and completeness are very important. Common errors that delay approval include,

You should carefully review all information before submission to ensure accuracy and completeness, as errors can significantly extend processing time.

After submitting your documents, banks conduct thorough due diligence to verify both the property value and legal status. This process involves two key components: property valuation and legal verification.

During property valuation, the bank appoints a professional evaluator to assess whether your property's market value aligns with the stated purchase price. This helps to protect both the lender and borrower from overpayment and ensures the collateral adequately secures the loan amount.

Legal verification involves a comprehensive review by the bank's legal team to confirm that the property has a clear title, the seller possesses legitimate ownership and authority to sell, no legal disputes or court cases affect the property, and all documentation is authentic and properly executed.

This verification process typically requires one to two weeks to complete. While waiting can be challenging for eager homebuyers, this thorough review is essential for protecting your investment and ensuring you are purchasing property free from legal complications.

After successful completion of all verification processes, the bank issues a formal loan approval and provides a sanction letter that includes details of your loan agreement. This document specifies the sanctioned loan amount, applicable interest rate (whether fixed or floating), loan tenure, monthly EMI amount, and all terms and conditions governing the loan agreement.

It is very important to read this sanction letter thoroughly and understand all its provisions before accepting. You should pay particular attention to clauses regarding consequences of payment default, prepayment or foreclosure penalties, processing fees and other charges, and any conditions or obligations you must fulfill.

If any terms are unclear to you or require clarification, do not hesitate to contact the bank and ask questions. Understanding your contractual obligations before signing prevents future disputes and ensures you are fully aware of your commitments.

The final stage of the home loan process involves the disbursement of the approved loan amount. In standard practice, banks do not transfer the loan amount directly to the borrower. Instead, they transfer the amount directly to the property seller. This direct payment mechanism protects all parties and ensures funds are used for their intended purpose.

Disbursement occurs through one of two methods, depending on the property status. Lump sum disbursement provides the full amount at once for completed properties ready for immediate occupation. Similarly, staged disbursement releases funds in installments aligned with construction milestones for properties still under development.

After loan disbursement, your EMI obligation begins according to the agreed documentation. You must ensure you have arranged for the timely payment of your first installment and subsequent monthly payments to maintain a positive credit history and avoid penalties.

The loan amount you can get depends on several factors that financial institutions evaluate during the application process. Your monthly income plays an important role, as banks typically structure loans where the EMI represents approximately 40% to 50% of your gross monthly income.

Additionally, the Loan-to-Value (LTV) ratio, which represents the percentage of the property value that the bank will finance, typically ranges from 60% to 70% in Nepal.

For example, if you intend to purchase a property valued at NPR 10,000,000 (1 crore), and the bank offers a 70% LTV ratio, the maximum loan amount would be NPR 7,000,000.

The remaining NPR 3,000,000 is your down payment, which you must arrange from your personal savings or other sources. A larger down payment reduces your loan amount and consequently lowers your monthly EMI burden and total interest paid over the loan tenure.

First-time homebuyers often focus exclusively on the property price and loan amount, overlooking several additional costs that form an important part of the home-buying process. These expenses can pile up to certain amounts and should be factored into your budget from the outset.

These combined costs can easily amount to NPR 200,000 to NPR 300,000 or more, depending on your property value and specific circumstances. Budgeting for these expenses in advance prevents financial stress and ensures smooth completion of all purchase formalities.

Several crucial measures can improve your chances of home loan approval and help you get your approval on time.

Buying your first home is a significant financial commitment and a lifetime achievement in Nepal. The process for successful home loan approval includes establishing a realistic budget, followed by reviewing your income and financial obligations. Checking and improving your credit score before applying and conducting a thorough comparison of loan offers from different banks also helps to get your loan approved faster. Also, maintaining complete and accurate documentation is key to faster approval.

Platforms such as Saral Banking Sewa provide valuable resources, including interest rate comparison tools, credit assessment services, and centralized information about various banks' loan offerings, which help to make your loan process easier and faster.

With proper preparation, a clear understanding of the process, and access to reliable information, you can get past the home loan application process confidently and successfully secure financing for your dream home.

Most banks need you to earn at least NPR 25,000 to NPR 30,000 per month. But this changes based on how much you want to borrow. Bigger loans need bigger salaries.

The home loan approval usually takes 2 to 4 weeks in Nepal. This includes checking your documents, valuing the property, and legal verification. If you submit everything properly, it can be faster.

The maximum home loan tenure is 25 to 30 years, depending on the bank and your age. But remember that the longer period means smaller EMI, but you pay more interest overall.

Yes, collateral is required for taking a home loan. The house you're buying becomes the collateral. Some banks might ask for extra security or a guarantor, especially for big loans.

Yes, you can pay your loan early. But many banks charge a penalty if you pay early, especially in the first few years. Check your agreement first.

There's no single "best" bank. It depends on what you need: lower interest, faster processing, or better service. What works for your friend might not work for you. Therefore, always compare the interest rates of home loans from Nepalese banks, learn about their service charges, and choose the best option.

It's easy to compare home loan rates of banks in Nepal! Just use Saral Banking Sewa's loan comparison tool. You can see rates from all banks in one place. It saves you so much time.

The main documents required for a home loan in Nepal include a citizenship certificate, income proof, bank statements, and property papers. If you're self-employed, you'll need business documents too. Each bank has slightly different requirements.

You can apply for a home loan online through the bank's official website or visit the branch in person. Most big banks now have online applications. Pick whichever is more comfortable for you.

The home loan interest rate of Nabil Bank varies depending on factors like loan amount, tenure, and market conditions. Typically, rates in Nepal can change frequently based on the base rate and bank policies. To get the latest and most accurate interest rate, it’s best to compare current rates using platforms like Saral Banking Sewa, which shows updated rates from multiple banks in one place.

There is no single “best” bank for everyone when it comes to home loans in Nepal. The right choice depends on your financial situation, interest rate preferences, loan flexibility, processing fees, and repayment options. Instead of choosing blindly, it’s smarter to compare home loan offers from different banks using Saral Banking Sewa. This helps you find the most suitable option based on your needs and budget.