Imagine applying for a loan to buy a home, expand your business, or meet an urgent financial need, only to be told that your application cannot proceed because your name appears in the CIB database. For Many people in Nepal, hearing the term CIB for the first time can be confusing and even alarming.

Does it mean you are blacklisted? Can you still get a loan? How can you check your status?

Understanding your CIB record is important before applying for any loan or credit facility. The Credit Information Bureau (CIB) maintains information on borrowers’ credit histories, and banks and financial institutions often review it when evaluating loan applications. A poor credit record can affect your ability to access financing, while a healthy credit profile can improve your chances of approval.

In this blog, you’ll learn what CIB is, what it means to be blacklisted, how to check your CIB status in Nepal, and the practical steps you can take to improve your credit report and maintain a strong financial reputation.

The CIB is a system that records and maintains the credit history of individuals and businesses in Nepal. It collects information about loans, repayments, and other credit-related activities from banks and financial institutions.

Its main purpose is to help lenders make responsible lending decisions. Before approving a loan, banks often review a borrower’s CIB record to assess their repayment history and creditworthiness.

By providing reliable credit information, CIB promotes responsible borrowing, reduces lending risks, and supports a healthy financial system in Nepal.

Banks and financial institutions use CIB to better understand a borrower’s credit history before approving loans or other credit facilities. By reviewing past borrowing and repayment behavior, they can assess whether an applicant is likely to repay a new loan on time.

A strong repayment history can improve the chances of loan approval, while missed or overdue payments may raise concerns. This helps lenders manage risk, make informed decisions, and promote responsible lending practices.

No, CIB and a credit score are not the same thing. CIB is a credit information system that stores and provides borrowers’ credit records, while a credit score is a numerical value that reflects a person’s creditworthiness based on their financial and repayment history.

In simple terms, CIB provides credit information, and a credit score is one way to analyze and summarize that information.

Being blacklisted by CIB generally means that a borrower has a history of serious repayment issues, such as failing to repay a loan according to agreed terms. When this happens, the borrower records a loan according to the agreed terms. When this happens, the borrowers may be flagged, making lenders more cautious about providing new credit.

However, being blacklisted is not a permanent situation. In many cases, borrowers can take steps to resolve their financial standing over time.

If you are blacklisted, obtaining new loans, opening deposit accounts, or credit facilities may become more difficult. Banks and financial institutions may view you as a higher-risk borrower and may reject your application or impose stricter lending conditions.

A blacklisted status can also affect future financial applications, though the impact may vary depending on the lender’s policies and the circumstances surrounding the credit issue.

Yes, both individuals and businesses can appear in CIB records if they have significant repayment problems.

While the basic process is similar, businesses are often evaluated using additional factors such as financial performance, cash flow, and overall business credit history. Maintaining a strong repayment record is important for both personal and business borrowing.

There are several reasons why an individual or business may be blacklisted by CIB. In most cases, it is linked to unresolved credit or repayment issues. Understanding these common causes can help borrowers avoid financial difficulties and maintain a healthy credit record.

Missing Loan Installments for a Long Time

Regularly missing loan installments is one of the most common reasons borrowers face problems with their credit records. While an occasional delay may not have a major impact, repeated missed payments over an extended period can signal financial distress and negatively affect a borrower’s standing with lenders.

A loan default occurs when a borrower fails to repay a loan according to the agreed terms, and the debt remains unpaid for an extended period. This is different from occasional late payments, which may happen due to temporary financial challenges. Long-term non-payment is considered a serious issue and can lead to blacklisting.

Cheque bounce incidents can also create financial concerns, especially when cheques issued for loan repayments or other financial obligations are returned for insufficient funds. Such cases may raise concerns about a borrower’s financial reliability and can affect their credit record.

Many people are unaware that serving as a loan guarantor comes with significant responsibility. If the primary borrower fails to pay the loan and the obligation remains unresolved, the guarantor may also face financial consequences. Before agreeing to become a guarantor, it is important to fully understand the associated risks and responsibilities.

Unresolved disputes related to loan settlements, outstanding dues, or repayment agreements can also lead to issues in a borrower’s financial record. Addressing such matters promptly and maintaining clear communication with the financial

If you're planning to apply for a loan, it's a good idea to check your CIB status beforehand. This can help you identify potential issues early and avoid surprises during the loan approval process. Here are the most common ways to check your CIB record in Nepal.

One of the easiest ways to check your CIB status is to contact the bank or financial institution with which you have an existing loan or banking relationship.

The institution may verify your identity and request information such as your citizenship number, account details, or loan account information. Based on their internal processes, they can guide you on whether there are any issues with your credit record and what steps to take next.

You can also request your credit information report directly through the Credit Information Bureau (CIB) Nepal. This report provides details about your credit history, including active loans, repayment records, and other relevant credit information.

The process typically involves submitting an application, verifying your identity, and providing the required supporting documents. Once approved, you can review your report and address any discrepancies or outstanding issues.

When requesting a CIB check or credit report, you may be asked to provide:

Having these documents ready can help speed up the verification process.

Both online and offline methods can help you understand your credit standing, but they differ in convenience and accessibility.

For the most accurate assessment of your credit history, obtaining an official credit report remains the most reliable option. However, online credit-checking tools can be a useful first step in understanding your financial health before applying for a loan.

One of the most common questions borrowers have is how long their name remains on the CIB blacklist. The answer depends on the nature of the credit issue and how quickly it is resolved. In many cases, the status can change once outstanding obligations have been settled and the necessary updates have been processed.

There is no single timeline that applies to everyone. The duration a borrower remains affected can vary depending on factors such as the amount owed, the type of credit issue, and how quickly repayments or settlements are made.

Verification and record-updating processes may also influence how long it takes for changes to appear in the system.

Repaying outstanding dues is an important step, but the update may not appear immediately. Financial institutions generally need to verify the repayment and submit updated information through the appropriate channels.

For this reason, borrowers should follow up with their bank or financial institution after resolving the issue and confirm that the necessary updates have been processed.

Borrowers should have realistic expectations regarding record updates. While some changes may be reflected relatively quickly, others can take additional time due to verification and administrative procedures.

If you have recently cleared an outstanding obligation, it is a good practice to periodically check your credit information and maintain communication with the relevant financial institution until the update is confirmed.

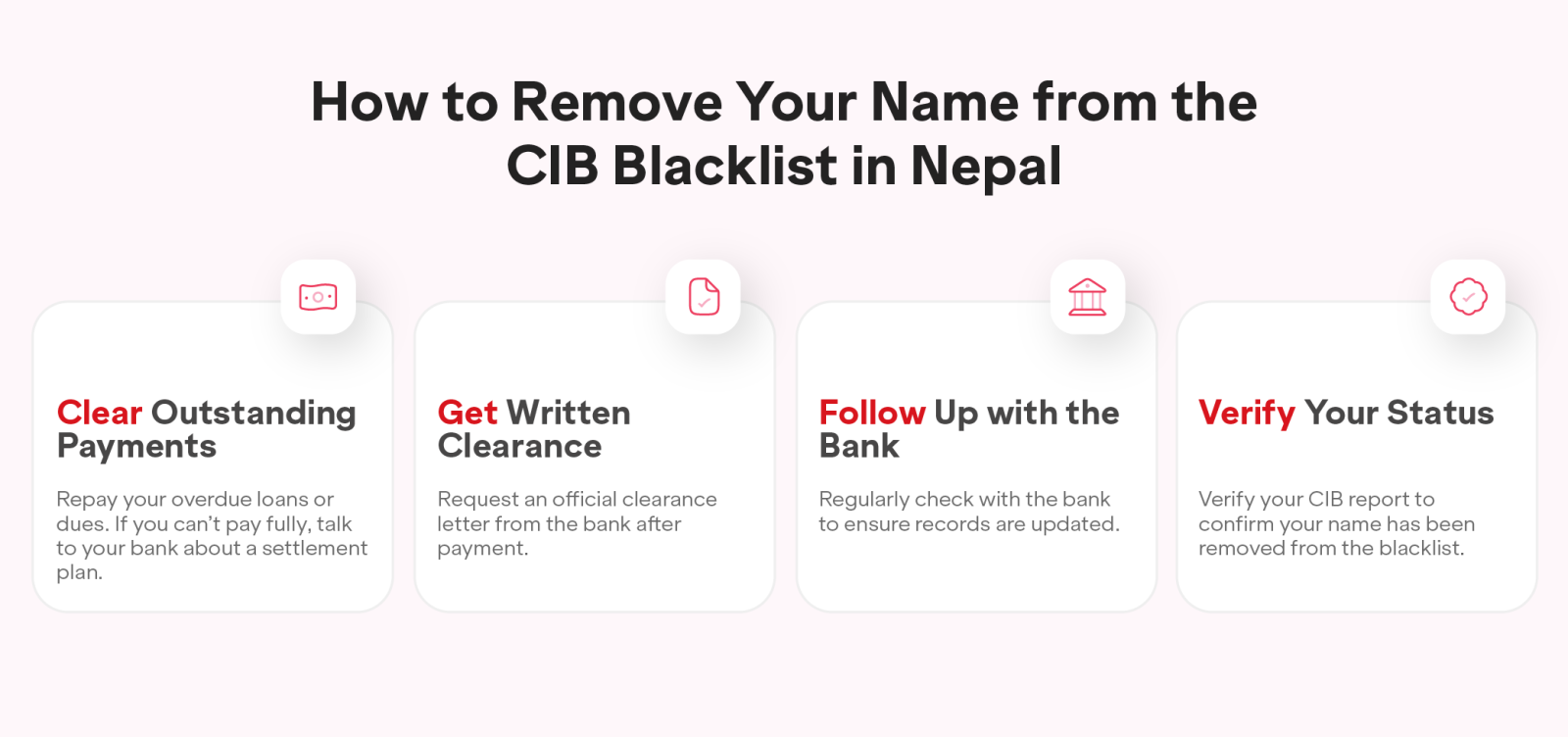

If your name appears on the CIB blacklist, the good news is that the situation can often be resolved. The key is to address the underlying issue, work closely with your lender, and ensure that your records are properly updated. Here are the steps you can take.

The first and most important step is to repay any overdue loan installments, outstanding balances, or other financial obligations that led to the issue. If you are unable to make a full payment immediately, discuss possible settlement or repayment options with your lender.

Maintaining open communication with the bank or financial institution can help you understand the requirements and resolve the matter more efficiently.

Once the outstanding amount has been cleared or a settlement has been completed, request written confirmation from the lender. This document serves as proof that your obligations have been fulfilled and can be useful if questions arise later.

It is also a good idea to keep copies of payment receipts, settlement agreements, and clearance letters for your records.

Resolving the payment issue is only part of the process. Financial institutions may need time to verify the repayment and update the relevant records.

Following up with your lender helps ensure that the necessary updates have been submitted and that there are no outstanding issues delaying the process.

After the updates have been processed, check your credit information to confirm that your status has been updated correctly. This step is especially important if you plan to apply for a new loan or credit facility in the near future.

Verifying your records can help you avoid unexpected delays and give you confidence that your credit profile accurately reflects your current financial situation.

A healthy credit profile can improve your chances of getting loans approved and help you build a strong financial reputation. By developing good financial habits, you can reduce the risk of credit-related problems and maintain a positive record over time.

One of the simplest and most effective ways to maintain a healthy credit profile is to pay your loan installments on time. Consistent, timely payments show financial responsibility and help build trust with lenders.

To avoid missing due dates, consider setting reminders on your phone, enabling automatic payments where available, or creating a monthly budget that prioritizes loan repayments.

Borrowing can be useful when managed responsibly, but taking on more debt than you can comfortably repay may lead to financial stress. Before applying for a new loan, evaluate your income, expenses, and existing financial commitments.

Using credit wisely and avoiding unnecessary borrowing can help you maintain better control of your finances and protect your credit record.

Many people agree to become loan guarantors for friends, relatives, or business associates without fully understanding the responsibility involved. As a guarantor, you may be held accountable if the primary borrower fails to repay the loan.

Before signing as a guarantor, make sure you understand the terms, assess the borrower's ability to repay, and carefully consider the potential financial risks.

Maintaining organized financial records is an important but often overlooked habit. Keep copies of loan agreements, repayment receipts, settlement documents, and any correspondence with financial institutions.

Proper documentation can help resolve disputes, verify completed payments, and provide evidence of financial settlements whenever needed. Having these records readily available can save time and prevent complications in the future.

Understanding your CIB status is an important part of managing your financial health in Nepal. While being blacklisted can create challenges when applying for loans or other credit facilities, it is often the result of specific repayment or financial issues that can be addressed and resolved.

Regularly checking your credit information helps you identify potential problems early, correct inaccuracies, and take the necessary steps to maintain a strong credit profile. Whether you are planning to apply for a personal loan, home loan, business loan, or any other form of credit, knowing your CIB status beforehand can help you avoid unexpected delays and improve your chances of approval.

Planning to apply for a loan in Nepal? Check your CIB status first, clear any unresolved issues early, and build a healthier credit profile for smoother financial opportunities ahead.

Curious about your credit score? Check it with Saral Banking Sewa's Credit Score Checker and get a quick estimate. It's a simple way to estimate your score before checking the official report from CIB Nepal.

You can check your status by contacting your bank or financial institution or by requesting your credit information from the CIB Nepal report.

Karja Suchana Kendra Limited, also known as the Credit Information Bureau (CIB) of Nepal, is an organization that collects and maintains borrowers' credit information for banks and financial institutions.

It generally means there are serious repayment or credit-related issues associated with your financial record, which may affect your ability to obtain new loans.

The duration varies depending on the nature of the issue, repayment status, and the time required for verification and record updates.

Yes. In many cases, resolving outstanding dues or settlement issues and completing the required verification process can help update your status.

It may be difficult, as lenders often consider blacklisted borrowers to be higher risk. Approval depends on the lender's policies and your current financial situation.

Yes. If a borrower defaults on a loan and the obligation remains unresolved, the guarantor may also face credit-related consequences.

The fee for a personal credit history typically ranges from NPR 250 to 500, depending on the provider and report type. It's best to check with CIB Nepal or the relevant institution for the latest charges.

You may need a citizenship certificate or other identification document, loan account details (if applicable), and supporting verification documents.

Pay outstanding dues, settle unresolved obligations, maintain timely repayments, follow up with your lender, and regularly monitor your credit information to ensure records are updated correctly.