Are you planning to take a loan? Whether it's for a new home, a car, or starting your dream business, there is one invisible number that stands between you and your approval: your credit score.

A Credit Score is a digital record that tells banks how responsible you are with money. In Nepal’s fast-moving banking world, your credit score is your "Digital Certificate" of trust. A high score acts like a VIP pass, unlocking lightning-fast loan approvals, higher credit limits, flexible collateral options, and the power to negotiate lower interest rates that can save you lakhs in EMIs.

On the flip side, a poor history can land you on the "Blacklist," turning even a simple credit application into a major headache. So, in this guide, we’ll break down what a credit score is, how to check your score, what the 60 to 960 credit score means for your bank loans, and how the CIB uses your last 15 months of habits to judge your trust factor.

That’s not all, we will also explore the "hidden risks," tips to boost your score, and find the official way to check your report so you can take full control of your financial future.

A credit score is a numerical representation of your financial stability, primarily managed by the Credit Information Bureau (CIB) of Nepal. While the concept is similar to global systems like Fair Isaac Corporation (FICO) or Credit Information Bureau India Limited (CIBIL), the infrastructure in Nepal has specific characteristics.

While international markets often use a range of 300 to 900, Nepal’s evolving financial landscape follows a unique scale:

This score is based on your credit behavior over the last 15 months, which is managed by CIB, which acts as the national repository for credit information from all banks and financial institutions (BFIs).

In Nepal, your financial reputation is managed by CIB. Think of the CIB as a central, neutral library that keeps a record of every individual's borrowing behavior. They don't just guess your score; they act as a data hub where all licensed banks and financial institutions report your activity every month.

Whether you’ve paid your EMI on time or missed a credit card payment, it all gets logged here to create your "financial report card." By centralizing this data, the CIB helps banks decide if you are a "safe bet," ensuring that responsible borrowers get better deals while maintaining the overall stability of Nepal's banking system.

Having a high credit score in Nepal is like carrying an “Exclusive Card" in the banking world. It proves to lenders that you are a person of your word when it comes to money.

The credit score is your most valuable financial asset, and here is why:

Calculating a credit score isn't based on a single event; rather, it’s a mathematical analysis of your entire financial behavior over the past 15 months. In Nepal, CIB calculates this score by analyzing several key factors reported by your banks.

The major factors that determine whether your score climbs toward 960 or slips toward 60 include:

This is the most important factor in the calculation. Banks usually want to know: Do you pay your debts on time?

This factor looks at how much of your available credit you are actually using, especially on credit cards.

The longer you are part of the formal banking system, the more data you provide to prove you are a reliable borrower through a history of successful repayments. This is why your first loan or credit card is an important step in building your "digital certificate of trust."

Banks like to see that you can handle different types of debt at once. A healthy mix might usually include:

Every time you apply for a loan, the bank makes a "Hard Inquiry" to the CIB. If you apply to five different banks in a short period, it suggests you might be in financial distress, which can temporarily lower your score and act as a red flag for lenders.

Understanding where you fall on this scale is essential before you apply for a loan, as each category changes how a bank looks at your financial health.

The Scoring Categories:

Quick Summary

| Score Range | Category | Bank’s View | Impact on Loan |

| 750-850 | Excellent | Star Borrower | Lowest Rates, Fast Approval |

| 650-749 | Good | Reliable | Standard Rates, Easy Approval |

| 550-649 | Average | Risky | Highest Rates, More Paperwork |

| 550 below | Poor | High Risk | Likely Rejection/ Blacklist |

Even if you have a high income, certain habits can act as "Invisible risks" for your credit standing. In the eyes of CIB, consistency is more important than the size of your paycheck.

The most common mistakes that can put you in the score down and how you can avoid them.

If your current score isn’t where you want it to be, don’t worry, a credit score is a living number, not a permanent scar. Because the system in Nepal focuses heavily on your behavior over the last 15 months, you can significantly transform your financial reputation with a year of disciplined habits.

Here is your roadmap to rebuilding and improving your credit score:

For a more detailed guide on improving your credit score, you can check these 7 proven steps to improve your credit score ratings in Nepal.

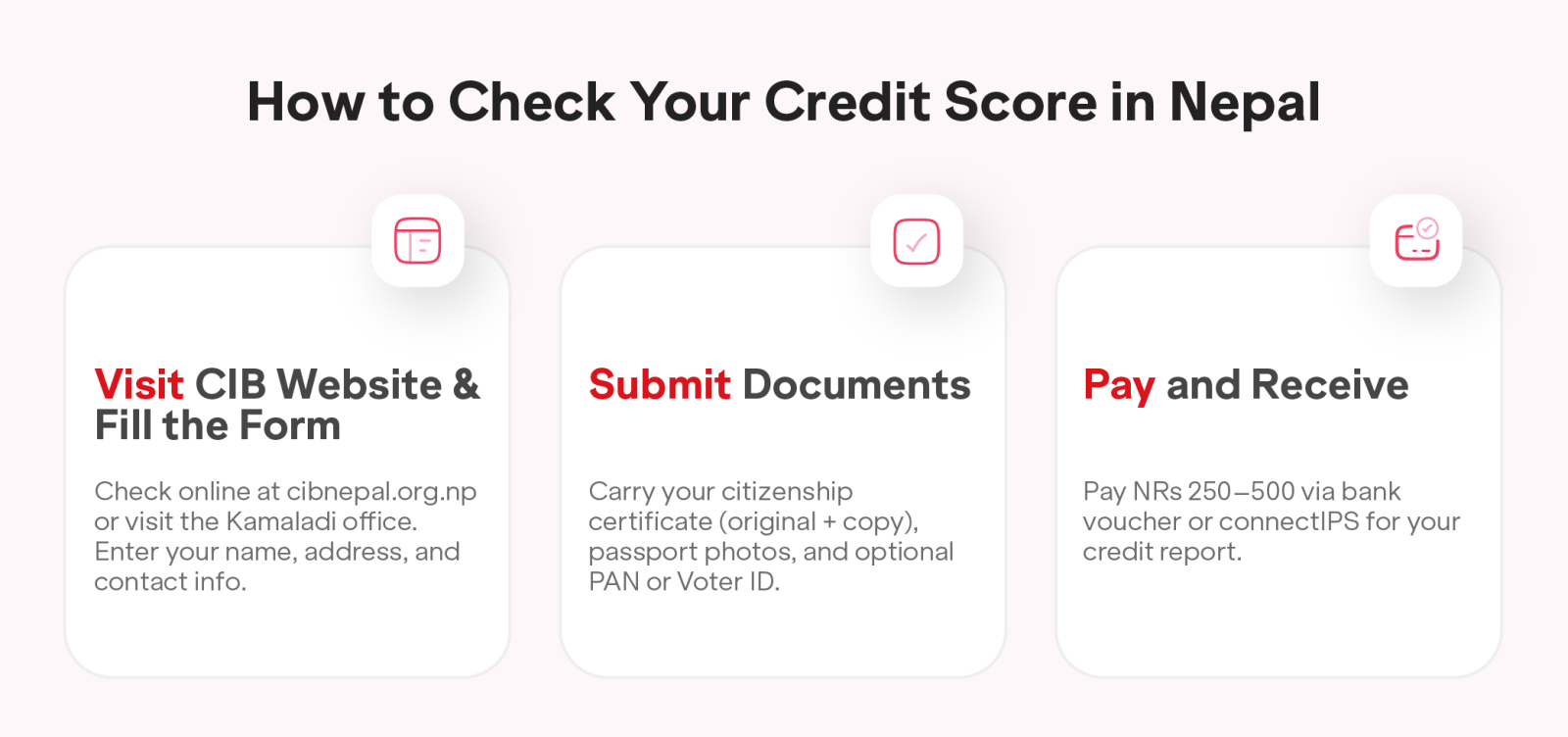

Knowing your credit score is the first step toward financial empowerment. The official way to check your credit score in Nepal is by visiting the official website of CIB.

Finally, once you receive your report, read it carefully. Look for:

Most people know that a good credit score helps you get a loan. But what many don't realize is that it also determines exactly how much that loan will cost you in the long run. In the financial world, your credit score is the primary tool banks use to set your interest rate.

Having an excellent credit score isn't just about pride; it’s about massive financial savings. Here is how it helps:

Before you walk into a bank and start a formal application, it is a smart move to get an estimate of where you stand. Saral Banking Sewa offers a specialized tool to help you understand your creditworthiness from the comfort of your home. Use the Saral Credit Assessment Tool to get a better idea of your financial health before making your big move.

Applying for a loan is a major life decision. A little preparation today can save you from years of high interest and financial stress tomorrow. Before you sign on the dotted line, follow these important steps to ensure you are getting the best deal possible.

In Nepal's changing financial world, your credit score is more than just a number; it is your financial reputation. Think of it as your digital resume that tells banks exactly how much they can trust you.

As we’ve explored, maintaining a high score is the key to unlocking faster loan approvals, higher credit limits, and lower interest rates that can save you lakhs of rupees over time. Whether you are dreaming of a new home, a vehicle, or a business venture, your past financial behavior will pave the way for your future success.

Remember, a credit score is not static. By practicing good financial habits, paying your EMIs on time, keeping your credit usage low, and avoiding unnecessary loan applications, you can build a "Digital Certificate" that opens doors across the banking sector.

Take the first step today. Before you apply for your next loan, get a clear picture of where you stand.

Use the Saral Banking Sewa's Credit Score Checker to assess your creditworthiness from the comfort of your home and ensure you’re always in the best position to negotiate.

While there is no "official" minimum mandated by the central bank, most commercial banks in Nepal prefer a score of 650 or above.

2. How can I improve my credit score in Nepal?

You can improve your credit score in Nepal by paying all loans and bills on time, reducing credit card use, and avoiding too many loan applications. Also, keep old accounts active and maintain low debt. These simple steps can help you improve your credit score in Nepal.

3. Can I get a loan with a low credit score?

Yes, but it is much harder. With a low score, banks may ask for higher collateral, charge a higher interest rate, or require a strong guarantor. Some digital-first lenders or microfinance institutions might consider your application, but the terms will likely be less favorable than for someone with a high score.

Check it once a year or at least 3–6 months before applying for a major loan (like a home or business loan). This gives you enough time to fix any mistakes or improve your score before the bank sees it.

There are no "instant" fixes because the CIB tracks your behavior over a 15-month window. However, you can see a significant boost in 6 to 12 months by paying all your EMIs exactly on time and keeping your credit card usage below 30%.

Once you settle your debt and your bank submits a No Objection Certificate (NOC) to the CIB, it typically takes 30 to 90 days for the records to be updated and your name to be officially removed from the blacklist.

Currently, official reports are primarily issued through physical visits to the CIB office or through your bank. However, you can get an instant estimate of your credit standing using the Saral Banking Sewa Credit Score Checker. It’s a fast, user-friendly way to understand your creditworthiness from home.

In Nepal’s 60–960 range, a score between 650 and 749 is considered "Good." If you are above 750, your score is "Excellent," making you a top-tier candidate for the best banking deals.

A score below 550 is generally considered poor. This is usually the result of multiple late payments, check bounces, or being previously blacklisted. If you are in this range, you should focus on credit repair before applying for new debt.