Imagine you are standing at the billing counter of a busy supermarket. Your shopping cart is piled high with groceries, a pair of new shoes, and a few household essentials. The cashier rings up your total, looks up, and asks the ultimate modern question: “Card or QR? You open your wallet and freeze. You have two identical-looking banking cards: one is a debit card, and the other is a credit card.

If you have ever been confused at the cash counter, you are not alone. While these cards look like twins, they handle your money in opposite ways: one spends your actual savings, while the other is a temporary loan from the bank.

This guide will directly break down the differences between debit and credit cards and how they operate under Nepal Rastra Bank (NRB) guidelines. We will look into the real-world pros and cons, and the sneaky hidden fees you need to watch out for in Nepal. By the end, you'll know exactly when to swipe which card so you can avoid debt, maximize your perks, and make the smartest moves for your money.

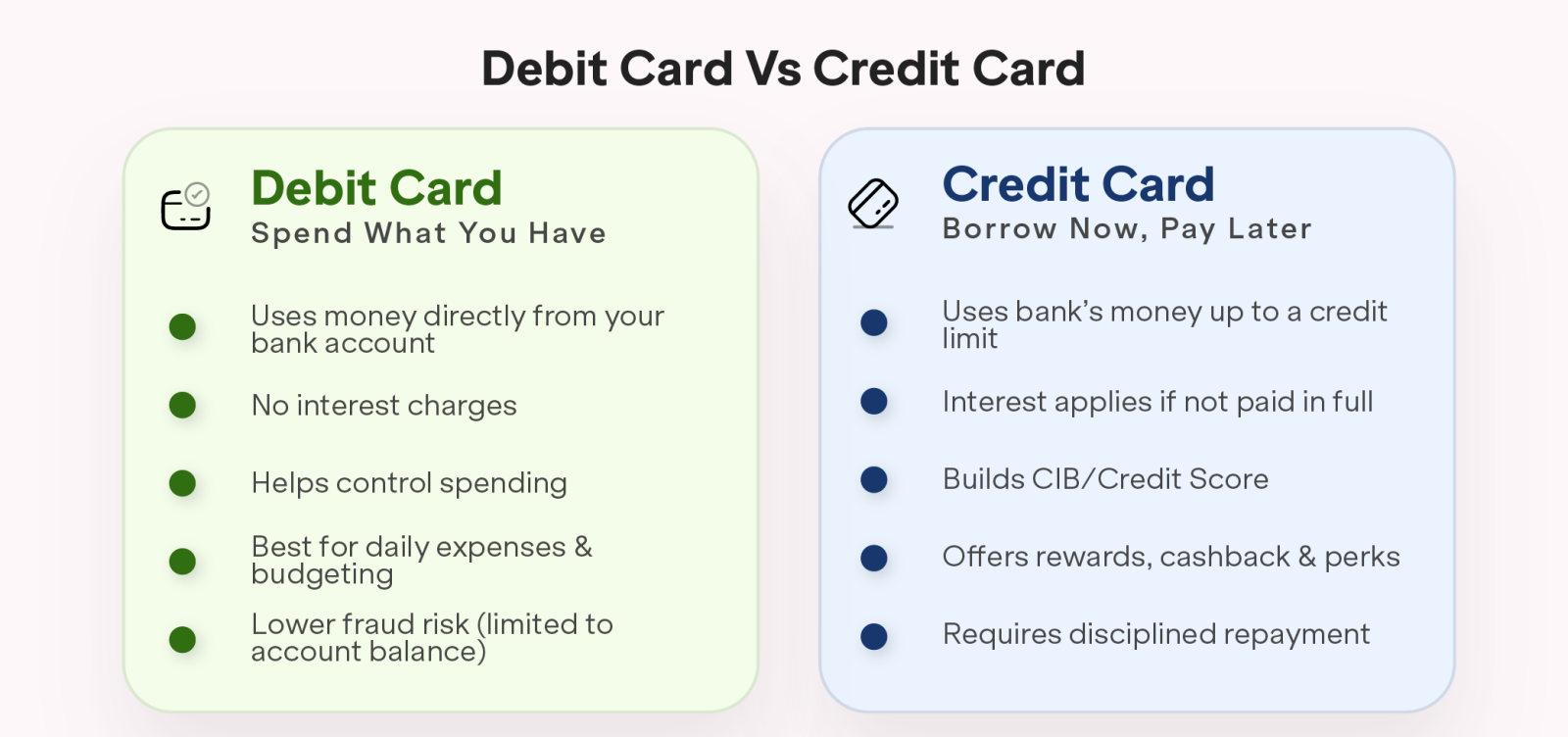

A debit card is a payment card issued by a bank and linked directly to a current or savings account, so whenever you spend with it, the amount is instantly deducted from the account. In Nepal, debit cards are primarily used for ATM cash withdrawals, in-store purchases by swiping or tapping at retail shops, restaurants, supermarkets, and digital & Online payments for utilities, recharging local wallets, or shopping on domestic e-commerce sites.

Usually, Nepalese Banks offer three types of Debit cards:

Because a debit card is linked directly to the account holder’s savings or current account, every time you make a transaction, you are spending your own hard-earned money in real time. This makes it incredibly accessible, and debit cards are far more readily available than credit cards in Nepal; almost anyone who opens a basic bank account is automatically eligible to receive one without needing to provide proof of income.

This system offers a huge financial advantage; there is virtually no risk of debt, as you can only spend what you already have, making it practically impossible to fall into a debt trap or take on high-interest loans. Purchasing power is strictly tied to your own financial reality, so if you do not have sufficient funds in your account, your card will automatically decline the moment you try to use it, keeping you safely within your means.

The only real trade-off is that aside from occasional festive cashback campaigns or merchant discounts arranged by your bank, you generally won't earn extensive reward points, air miles, or premium lifestyle benefits just for swiping.

A credit card allows you to make purchases without having immediate funds in your bank account, but you must pay back the amount charged, plus any fees, later. In Nepal, credit cards are commonly used for large purchases on EMI, online shopping, and emergencies. Banks set a spending limit based on your income, and you receive a monthly statement detailing your transactions and minimum payment.

Nepal's commercial banks offer different types of credit cards:

The credit card business operates on the “buy now, pay later” model, which allows customers to make purchases instantly, even if their bank account is empty, because the bank pays the merchant upfront on the customer's behalf. They offer financial flexibility, reward points, and a built-in safety net, usually valid for domestic use and in countries like India and Bhutan.

One can enjoy 15 to 45 days of interest-free credit from the billing date. If one cannot pay the full amount, banks allow them to pay a minimum percentage or a fixed amount to keep their account in good standing. Also, customers can withdraw cash from an ATM, but under Nepal Rastra Bank directives.

Credit cards are also highly valued for their ability to earn rewards and cashback, allowing you to accumulate points on everyday purchases that can later be redeemed for gift vouchers, flight discounts, or waivers on your annual fees. Furthermore, one of the most valuable features of credit cards in Nepal is the EMI option.

This feature allows users to break down large, expensive purchases such as smartphones, laptops, or home appliances into manageable, bite-sized monthly payments over 3 to 18 months, often at 0% interest through partner merchants.

Both Debit and Credit cards give a smooth, cashless way to shop and pay bills in Nepal, but they operate on opposite financial principles. While debit and credit cards directly deduct money from your own bank account, a credit card is a short-term loan facility that lets you borrow money up to a set limit from the bank, which you must repay later.

To help you see how they stack up side-by-side, here is a comprehensive breakdown of the key differences between the two:

| Features | Debit Card | Credit Card |

| Source of Money | Own bank savings/current account. | Borrowed Money |

| Spending limit | Available balance | Credit Limit |

| Interest charges | No | Yes if unpaid |

| Rewards | Limited | More rewards |

| Credit Score Impact | Usually no | Yes |

| Overspending Risk | Lower | Higher |

| Approval Process | Easy | Requires eligibility |

| EMI Facility | Limited | Common |

| Best for | Budgeting | Flexible spending |

When it comes to deciding whether a debit card or a credit card is the better choice, there is no single right answer on which one is better, as one card is not inherently better than the other; instead, the right choice depends entirely on users' financial discipline, their current financial goals, and how they prefer to manage their monthly budget.

A debit card is the best choice for everyday budgeting, small, routine purchases, and teaching teens and young adults how to manage money without risking debt. Since there are no interest charges or strict eligibility requirements, it’s a simple, stress-free tool for anyone, including those rebuilding their credit.

Most importantly, always use your debit card for ATM cash withdrawals to avoid the huge fees and immediate interest that come with using a credit card. For example, paying for groceries at the supermarket, splitting a bill with friends at a local restaurant, or making quick daily purchases at a neighborhood store.

A credit card can be a powerful tool when used responsibly, helping to build a strong credit history for future loans in Nepal. It's ideal for large purchases due to added protections and the ability to earn rewards points or air miles on travel bookings.

Credit cards also provide better fraud protection for online shopping and serve as a safety net for unexpected expenses. By staying within your budget and paying the bill in full, you can leverage the bank's money while earning rewards on hotel stays, international flights, or subscription services.

Using both debit and credit cards for a purchase is actually the smartest way to manage money, since there is no restriction on using both. As explained earlier, a debit card is for daily use, an “everyday anchor” for routine expenses and small purchases to ensure staying strictly within budget.

Meanwhile, a credit card is for larger, planned purchases or travel to take advantage of reward points, EMI options, and better fraud protection. By balancing both, users get the full control of a debit card with all the premium perks and credit-building power of a credit card.

Following these practical, beginner-friendly tips, you can keep your savings secure and manage your budget effortlessly:

These tips will help you unlock all the perks of a credit card while keeping you completely safe from debt:

Eventually, the choice between a debit card and a credit card comes down to whose money you are spending. A debit card draws directly from your own savings, making it perfect for everyday budgeting and helping you stay out of debt. A credit card lets you borrow money from the bank up to a set limit, offering rewards, consumer protection, and the ability to pay later.

Because both cards serve completely different purposes, many successful money managers use them together, relying on a debit card for routine expenses and a credit card for larger, planned purchases. If you are ready to apply for a credit card, it is wise to check your eligibility with your bank first. You can quickly find out where you stand by using Saral Banking Sewa’s Credit Card Eligibility Checker tool to discover the best card options for your current financial status.

A debit card withdraws funds directly from a user's bank account, while a credit card allows users to borrow money from the bank up to a certain limit and pay it back later.

No, credit cards are generally safer for shopping. If fraud occurs, a credit card uses the bank's money and can be easily disputed, whereas a debit card hack allows thieves to drain your actual cash savings instantly.

Neither is always better; it depends on your habits. A debit card is better if you want to avoid debt and stick to a strict budget, while a credit card is better for earning rewards, splitting payments into EMIs, and building a credit history.

You will be charged heavy interest and late fees. Missed payments will also damage your credit score, and repeated defaults can land you on the CIB blocklist in Nepal.

You can instantly check your current qualification status by using the Credit Card Eligibility tool online to avoid unnecessary bank rejections.

A credit card is better. It offers excellent fraud protection, purchase insurance, and allows you to easily reverse fraudulent or incorrect online charges before any of your own money leaves your hands.

Yes. While regular credit cards require proof of independent income, students over 18 can get special student credit cards with a parent/guardian guarantee, or easily get a card by placing a lien on a Fixed Deposit (FD).

Yes, most commercial banks in Nepal charge a modest annual fee (typically between Rs. 300 and Rs. 500) to keep your debit card active.

It is very difficult to get a standard credit card with bad credit. However, you can secure a credit card by opening a Fixed Deposit (FD) account at the bank, which uses your deposit as collateral regardless of your credit history.

Should I close my credit card and just use debit?

You shouldn't close it unless you cannot control your spending. Keeping your oldest credit card account open and active helps you maintain a long, healthy credit history, which makes it much easier to get home or auto loans in the future.