The transition from cash-stuffed wallets to a quick tap-and-pay digital lifestyle is happening fast in Nepal. A credit card is a financial instrument that lets you borrow money from a bank up to a certain limit to make purchases, pay bills, or book flights, and then pay the bank back later.

In Nepal, having a credit card is no longer simply a luxury; it’s an effective way to build a strong credit history, manage emergency expenses, and enjoy exclusive rewards, EMI facilities, and discounts on everyday shopping.

If you are wondering how Nepali citizens can get their hands on one, you have come to the right place. In this blog, we will walk you through exactly what it takes to get a credit card in Nepal. We will cover the eligibility criteria among different professions, provide a foolproof document checklist, detail the step-by-step application process, and reveal the hidden fees you need to watch out for before you sign on the dotted line.

Eligibility is the first filter banks use to decide if you can responsibly handle a credit line. While the rules are guided by Nepal Rastra Bank (NRB), individual banks tweak them based on the applicant's profile.

If you have a steady 9-to-5 job, getting a credit card is usually straightforward, provided your income is verifiable.

For entrepreneurs, the bank looks at the stability of your business's cash flow rather than a fixed monthly paycheck.

Historically, students couldn't get credit cards. However, some banks in Nepal have introduced special provisions.

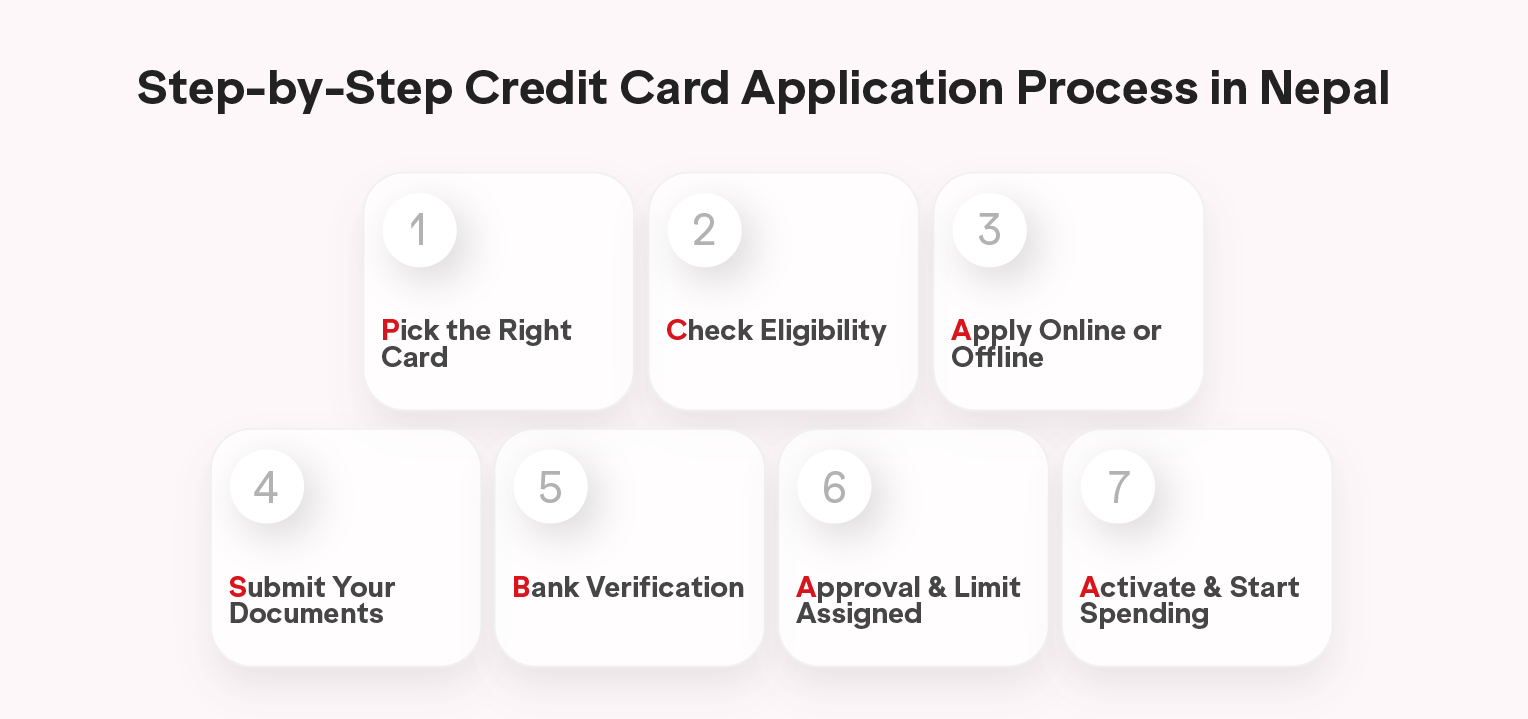

Having a "folder-ready" approach can speed up your application and prevent frustrating rejections. Here is exactly what you need to prepare:

Quick takeaway: Incomplete paperwork is the #1 reason for credit card rejection. Keep clear photocopies of these documents ready in a single folder before visiting the bank.

Do not just apply at the first bank you see. Research top banks offering credit cards in Nepal, such as Siddhartha Bank, Nabil Bank, Standard Chartered, Prabhu Bank, and NIC Asia.

Note: To compare the features and interest rates of various credit cards, use Saral Banking Sewa’s credit card comparison tool. Also, check the specific bank’s website for "Credit Card Offers" to catch the latest waiver promotions.

Before filling out forms, confirm whether you actually qualify.

Note: You can check your eligibility via our Saral Credit Card Eligibility tool. But before having to Some banks have special student or government employee cards with highly relaxed criteria. Ask the branch if you fall into these categories.

Online Application:

Note: We suggest you to compare and apply for credit cards directly on our Saral Banking Sewa.

Offline / Branch Application:

Gather your citizenship copy, passport photos, income proof, 6-month bank statements, and PAN/VAT certificates (if self-employed).

Note: Keep extra photocopies on hand and maintain a dedicated folder to avoid losing or misplacing any documents during transit.

Once submitted, the bank will conduct identity verification, income verification, and a Credit Information Bureau (CIB) check. They perform a background check to ensure the accuracy of your information. Some banks may call your office or home for clarification and it usually takes 2 to 7 business days.

If all requirements are met, the bank approves your application. Keep in mind that banks may offer a lower initial credit limit for first-time applicants to test their repayment discipline.

Note: Keep extra photocopies on hand and maintain a dedicated folder to avoid losing or misplacing any documents during transit.

Approved applicants will receive the physical card by mail or will be called to pick it up at the branch. Once in hand, you must activate the card using the bank's mobile app, internet banking portal, or at a designated ATM to set up your PIN.

When comparing credit cards, it is crucial to consider the annual fee and validity. Here is a realistic look at some of the best standard credit card offers available in Nepal:

| Bank Name | Typical Joining/Annual Fee | Interest Rate (Annually) | Card Validity |

| Rastriya Banijya Bank | NPR 750 | 18% | 5 Years |

| Nepal Bank Limited | NPR 750 | 24% | 3 Years |

| Nepal Investment Mega Bank | NPR 750 | 24% | 3 Years |

| Prime Commercial Bank | NPR 1,000 | 24% | 3 Years |

| Global IME Bank | NPR 1,000 | 24% | 5 Years |

(Note: Rates and fees are subject to change based on NRB guidelines and bank policies. Always verify the latest tariff sheets before applying.)

While a credit card is a powerful financial tool, it is essentially a short-term loan, not free money. If you pay your bills in full and on time, it costs you nothing in interest. However, if you miss a payment or only pay the "minimum amount," the costs can add up quickly through compounding interest and service fees. Here is a breakdown of what you need to know to stay ahead of the bank.

One of the best features of a credit card is the interest-free period, which typically spans 15 to 45 days. If you buy a product and pay your total outstanding bill before the statement due date, the bank charges you zero interest. You only pay interest if you carry a balance into the next month.

Picking the right credit card in Nepal is all about matching the features to your personal spending habits and lifestyle. Whether you are a frequent traveler looking for lounge access, a digital shopper seeking cashback, or a student wanting to build a credit score, the "best" card is the one that offers the most value for your specific needs.

Remember, a credit card is a tool for financial freedom when used responsibly. To save time and ensure you aren't overpaying on fees, we recommend using a comparison platform to evaluate the latest market offerings. By comparing interest rates, annual charges, and reward programs side-by-side, you can make a smarter choice and pick a card that truly fits your wallet.

Ready to find your match? Use Saral Banking Sewa’s credit card comparison features to filter through the latest credit card rates and benefits in Nepal, and apply for the one that suits you best today.

Yes, you can obtain a credit card without a job in some banks in Nepal but if and only if you have a Fixed Deposit (FD) account in that bank. Banks will issue a secured credit card against your FD, usually offering a credit limit up to 80-90% of your total deposited amount.

To get a credit card in Nepal, open an account with a bank, submit your citizenship, income proof, and bank statements. If you meet income requirements, the bank reviews your application and issues a card with a set credit limit.

A Rupee Credit Card is meant for domestic transactions in Nepal and India. A Dollar Card is a prepaid or credit card loaded with USD, strictly intended for international online purchases (like software or e-commerce) up to an NRB-approved yearly limit.

On average, it takes about 7 to 15 working days from the moment you submit a complete application. The timeline includes processing, CIB checks, approval, printing the physical card, and delivering it to your respective branch.

The minimum monthly salary required usually ranges from NPR 15,000 to NPR 25,000. However, this varies strictly by the bank and the specific card tier (Standard, Gold, or Platinum) you are applying for.

You must be a Nepali citizen between 18 and 60 years old. You need a stable, verifiable income source—either through at least 6 months of salaried employment or 1 to 2 years of registered business operations with proper tax clearance.

There is no single "best" bank; it depends on your needs. Siddhartha Bank and NIC Asia offer great digital experiences, Nabil and SCB provide excellent lifestyle rewards, and your own salary bank will likely offer you the fastest approval process.

You will need fundamental documents: a citizenship or passport copy, recent passport-size photos, verifiable income proofs (like salary slips or business audit reports), 6 months of bank statements, and a clean CIB history.

If you default on your credit card debt, the bank will charge heavy late fees and compound interest. Furthermore, you will be reported to the Credit Information Bureau (CIB) and blacklisted, preventing you from getting any future loans in Nepal.